[ad_1]

AlphaStreet Newsdesk powered by AlphaStreet Intelligence

Stock $47.97 (-2.8%)

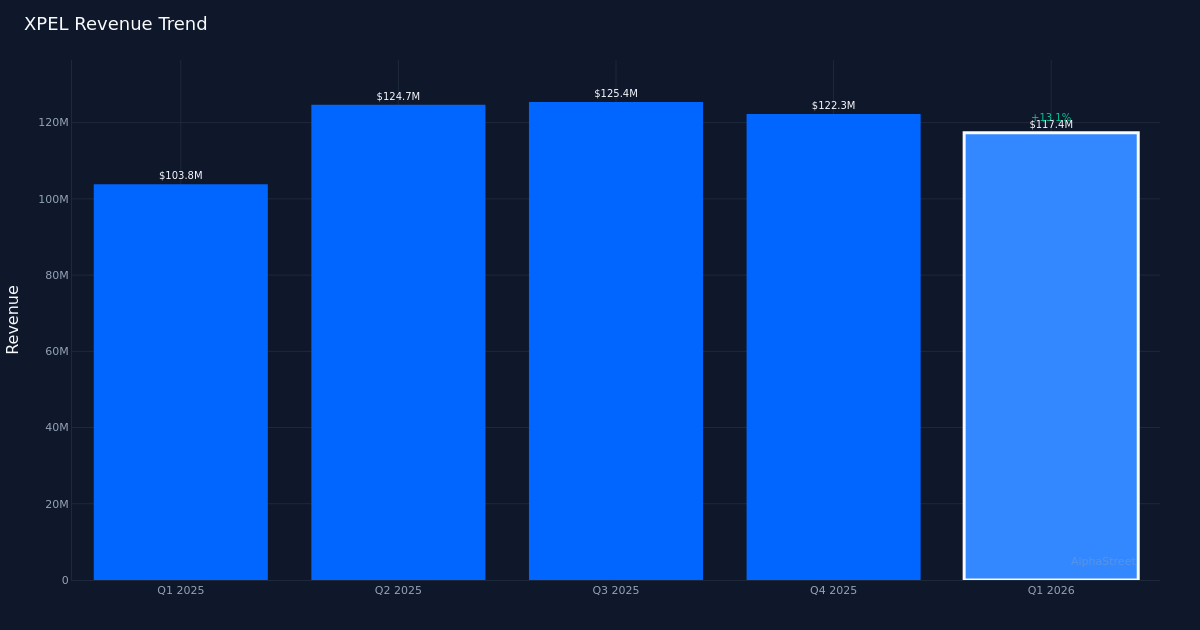

In-Line Quarter. Xpel, Inc. (NASDAQ: XPEL) delivered Q1 2026 diluted EPS of $0.37, matching analysts’ estimates, while revenue of $117.4M reflected solid year-over-year momentum in the company’s core protective film business. The auto parts specialist posted bottom-line profit of $10.5M as demand for paint protection and window tinting products continued to expand across both domestic and international markets.

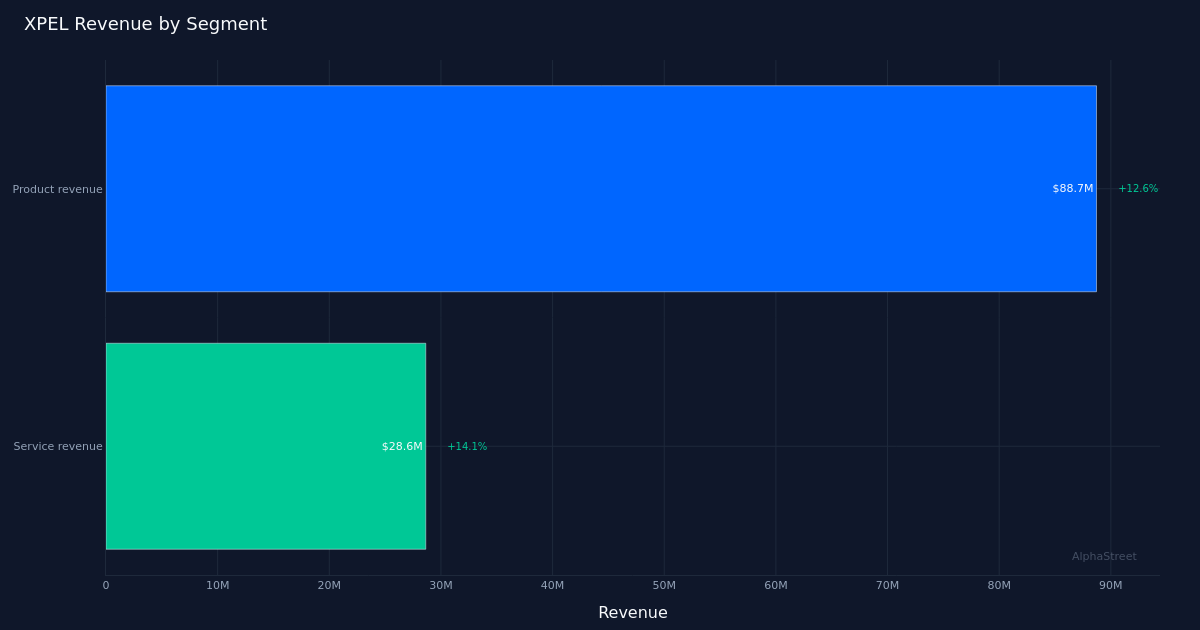

Revenue-Driven Growth. The quarter’s performance was anchored by genuine topline expansion rather than margin engineering, with revenue climbing 13.1% from $103.8M in Q1 2025. EPS advanced 19.4% year-over-year from the $0.31 posted in the prior-year period, suggesting operating leverage is building as the company scales. Product revenue led the way with $88.7M, up 12.6% year-over-year, underscoring healthy demand for Xpel’s flagship protective film offerings. This revenue-driven profile supports the quality of the earnings delivery, as growth appears tied to unit volume and market penetration rather than cost-cutting measures that can prove unsustainable.

Constructive Outlook. Management provided guidance for the next quarter calling for revenue of $135.0M to $137.0M, representing meaningful sequential acceleration from the $117.4M reported in Q1. This outlook signals confidence in the demand environment as we move deeper into the spring selling season, traditionally a stronger period for automotive aftermarket products. The midpoint of the range would imply roughly 16% sequential growth, suggesting the company expects installation activity to pick up as weather improves and consumer spending on vehicle customization remains resilient.

Muted Market Reaction. Despite the in-line print and optimistic forward guidance, shares traded down 2.8% to $47.97 in the session following results. The pullback likely reflects profit-taking after a recent run or investor expectations that had crept ahead of the company’s ability to surprise to the upside. With Wall Street consensus standing at 6 buy ratings, 1 hold, and 0 sell recommendations, the analyst community maintains a constructive stance on the stock even as near-term price action suggests some digestion of the results.

Fundamental Trajectory. The combination of double-digit revenue growth and accelerating EPS expansion demonstrates Xpel’s ability to convert market share gains into profitable growth. The 19.4% year-over-year EPS improvement outpacing the 13.1% revenue increase points to margin improvement and operational efficiency gains as the business matures. For a company serving the automotive aftermarket with consumable products that require periodic replacement and professional installation, this operating performance suggests the franchise value remains intact.

What to Watch: The gap between Q2 guidance and Q1 results will test management’s visibility into installer demand patterns and international expansion momentum, particularly as the company navigates a maturing domestic market while pursuing growth in emerging geographies.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.

[ad_2]

Source link