[ad_1]

AlphaStreet Newsdesk powered by AlphaStreet Intelligence

|Net Income $3.3M

Stock $17.78 (+12.2%)

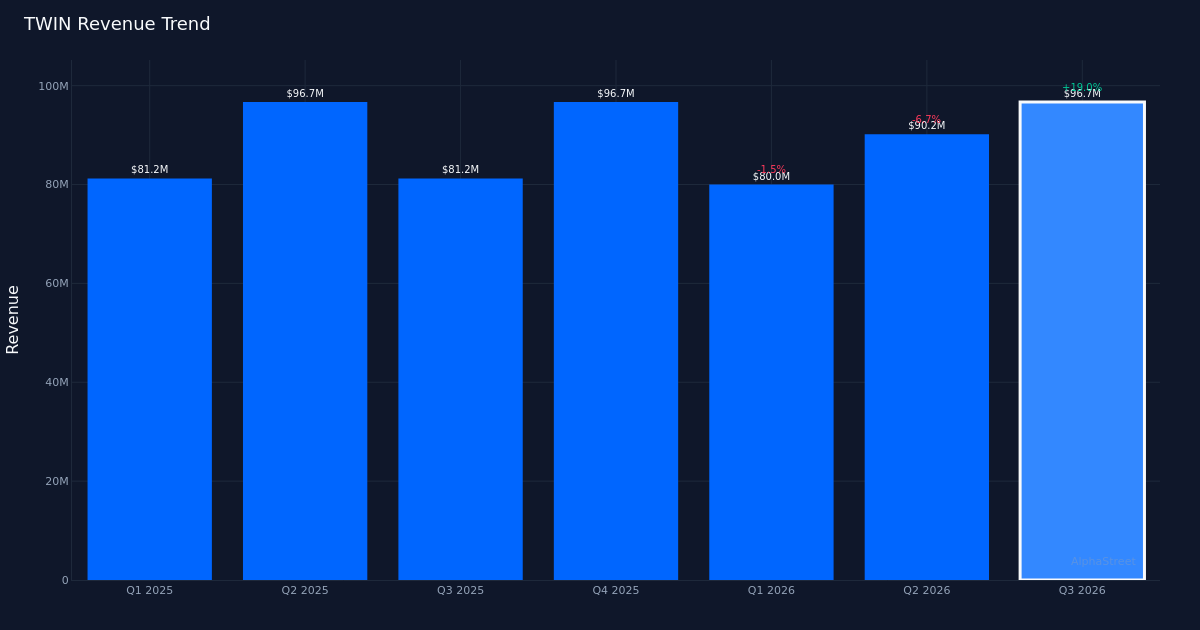

Mixed Quarter. Twin Disc, Incorporated (NASDAQ: TWIN) posted Q3 2026 diluted earnings of $0.23 per share, falling short of the $0.26 consensus estimate by 11.5%. Revenue of $96.7M met expectations, while net income reached $3.3M for the quarter. The stock surged 12.2% to $17.78 following the release, suggesting investors are looking past the earnings miss to focus on underlying momentum in the business.

Strong Year-Over-Year Trajectory. The specialty industrial machinery manufacturer demonstrated impressive growth fundamentals. EPS was up from a loss per share of $0.11 in Q3 2025, marking a dramatic return to profitability. Revenue increased 19.0% from the $81.2M recorded in the prior-year quarter, with organic sales growth contributing 7.0% to the top line. The swing to profitability alongside robust revenue expansion suggests the company has successfully navigated the operational challenges that plagued it a year ago.

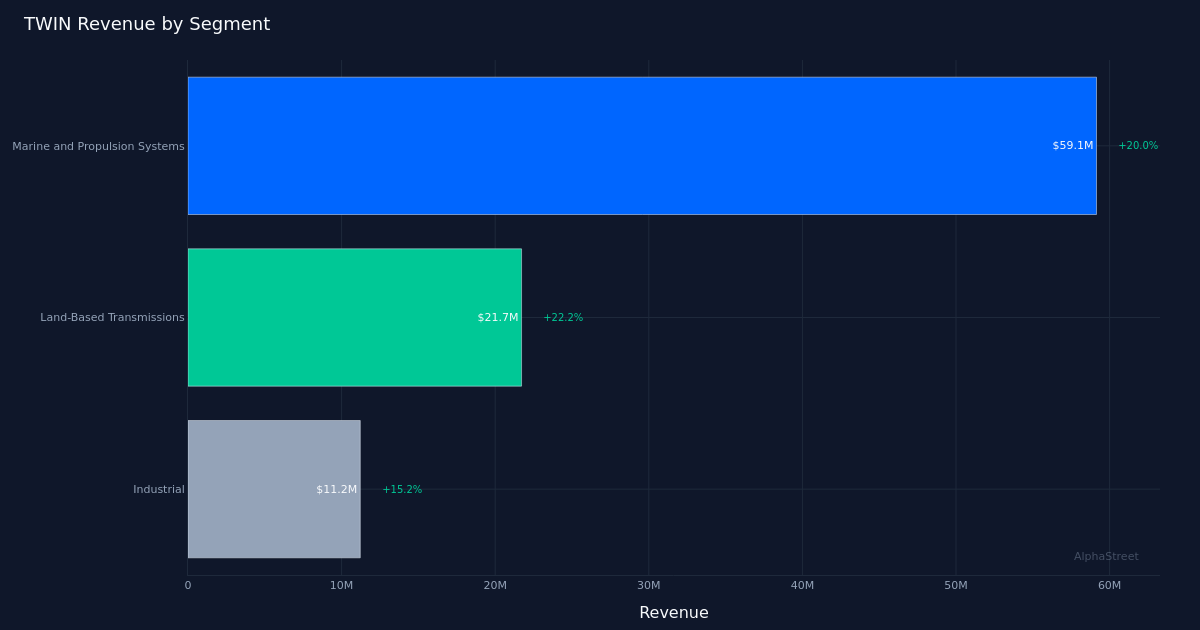

Marine Segment Drives. Marine and Propulsion Systems led the company’s performance with $59.1M in revenue, up 20.0% year-over-year. This segment represents the core of Twin Disc’s business, supplying transmission and propulsion systems to commercial and military marine markets. The 20.0% growth rate outpaced the company’s overall revenue increase, indicating market share gains or favorable industry conditions in maritime applications. The strength here appears revenue-driven rather than cost-engineering, lending credibility to the growth story.

Substantial Backlog. Twin Disc ended the quarter with a six-month backlog of $179.5 million, providing visibility into near-term production schedules and revenue conversion. For a specialty industrial machinery manufacturer, backlog serves as a leading indicator of manufacturing utilization and pricing power. The sizable backlog suggests demand remains healthy across the company’s end markets, supporting confidence in sustained revenue momentum through the coming quarters.

Market Reaction Favorable. The 12.2% stock price surge reflects investor conviction that the earnings shortfall was more timing-related than structural. With the shares climbing despite the bottom-line miss, the market appears to be rewarding the revenue performance and year-over-year profitability inflection. Wall Street maintains a constructive view with analyst consensus standing at 4 buy ratings, 1 hold, and 0 sell recommendations, underscoring institutional support for the Twin Disc investment thesis.

What to Watch: Conversion of the substantial backlog into revenue and whether organic growth can sustain mid-to-high single-digit rates as comparisons become more challenging. The ability to expand margins while maintaining top-line momentum will determine if Twin Disc can consistently meet or exceed consensus expectations in coming quarters.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.

[ad_2]

Source link