[ad_1]

Image source: Getty Images

Worries of a property market crash hurt housing stocks Taylor Wimpey (LSE:TW) until the end of last year. The company’s Q4 update didn’t produce the best numbers either. However, I still buy stocks for long-term growth and the potential to generate other income.

About Taylor Wimpey Plc

Last updated 2023-01-17, 11:12:16 GMT

Current price

117.85 p

Change it

0.50p (0.4%)

Close Price

117.35 p

Open Price

117.35 p

Offer

117.80 p

Inquire

117.90 p

Range of days

116.80p – 118.25p

Year Range

80.64p – 163.45p

Volume

2,882,690

Average Volume

13,190,013

District market

404,252,707,100.00p

Earnings Per Share

15.26 p.m

Hold up against the headwind

House prices are expected to fall by a double percentage point in 2023. This does not bode well for Taylor Wimpey shares. Additionally, December construction purchasing managers’ index (PMI) figures showed a contraction with the largest decline in new orders and purchasing activity in two years.

Despite that, the FTSE 100 stalwart still reported a higher than expected set of top-line figures there. Although the bottom-line number of the house builder will not be revealed until March, it is certainly positive to see it meet and even exceed some initial key performance indicators.

| Metric | 2022 | 2021 | Growth |

|---|---|---|---|

| Total done | 14,154 | 14,302 | -1% |

| Net personal reservation rates | 0.68 | 0.91 | -25% |

| Cancellation rates | 18% | 14% | 4% |

| Average selling price | £313k | £300k | 4% |

| Book value | £1.94bn | £2.55bn | -24% |

| Total land bank | 144k | 145k | -1% |

In fact, the company is doing well against some of its peers. This is particularly the case in areas such as net personal reservation rates (sales per outlet per week).

| House builder | Net personal reservation rates |

|---|---|

| Taylor Wimpey | 0.68 |

| Barratt | 0.44 |

| persimmon | 0.69 |

A solid foundation

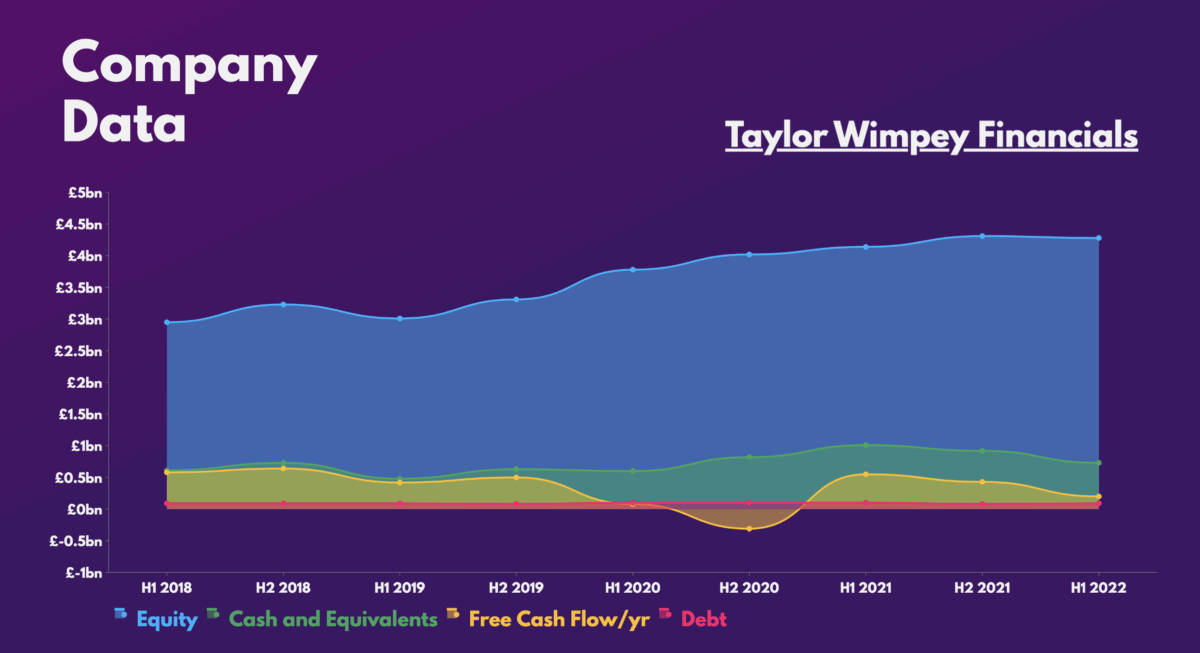

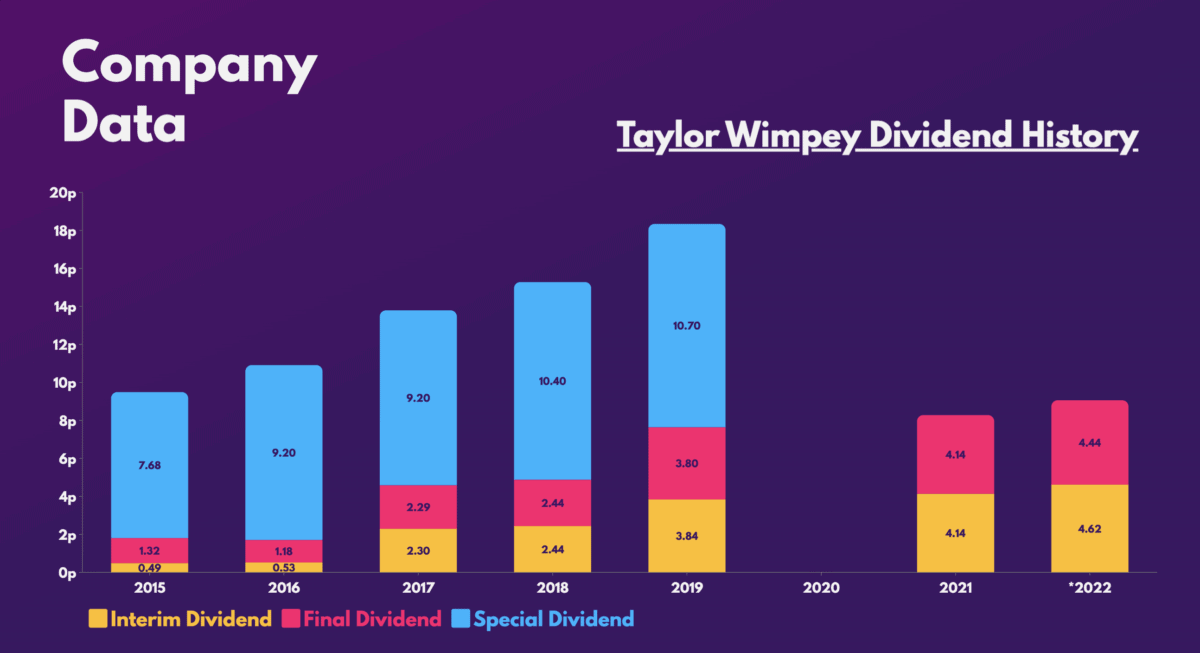

The company ended 2022 with more net cash than expected, and even saw operating margins widen. With a debt-to-equity ratio of 2% and an impressive dividend cover of 2.1 times, it certainly lays a solid foundation for an investment in Taylor Wimpey shares.

This is good news for earnings as well as dividends. Taylor Wimpey has a distinguished history of growing dividends. And unlike his friend persimmon, Management has not shown rebasing of high payouts. However, a prolonged period of lower house prices and sub-par free cash flow could force the council’s hand.

However, it should be noted that even in such cases, the developer has a safe dividend policy. The constructor aims to pay a dividend of at least 7.5% of net assets, or at least £250m a year. Buying Taylor Wimpey shares today would still yield a minimum dividend of 6.1%, even in the group’s worst-case scenario.

Rebuild it bigger

Having said that, there are some things to be optimistic about. For one, house prices are not necessarily falling as much as anticipated due to the limited housing supply. Additionally, Taylor Wimpey has a healthy exposure to second-time buyers (40%). This should allow to prevent the decline in the first buyer base (35%) due to concerns about affordability. And there is another £20m of cost savings to come with building inflation rate out costs. Meanwhile, mortgage rates are also falling.

All of these should be gradual tailwinds over the next few years. And although home prices are forecast to continue to decline in the short term, buyer intent remains firm, according to CEO Jennie Daly. With construction activity typically the first sector to benefit when the economy picks up, Taylor Wimpey shares are in a prime position to capitalize on this, if buyer intent remains strong.

No wonder I like it Jefferies and Taylor Wimpey’s Liberum rates indicate ‘buy’, with the latter even suggesting a 25% rise this year. So, given the good valuation and strong dividend yield, I would buy the stock if my broker of choice launched UK stocks on the platform.

| Metric | Multiples of value | Industry average |

|---|---|---|

| Price-to-earnings (P/E) ratio. | 7.2 | 10.7 |

| Price-to-sales ratio (P/S). | 1.0 | 0.8 |

| Price-to-book (P/B) ratio. | 1.0 | 0.9 |

[ad_2]

Source link