[ad_1]

AlphaStreet Newsdesk powered by AlphaStreet Intelligence

Stock $15.33 (+56.9%)

EPS YoY +114.3%|

|Net Margin -6.4%

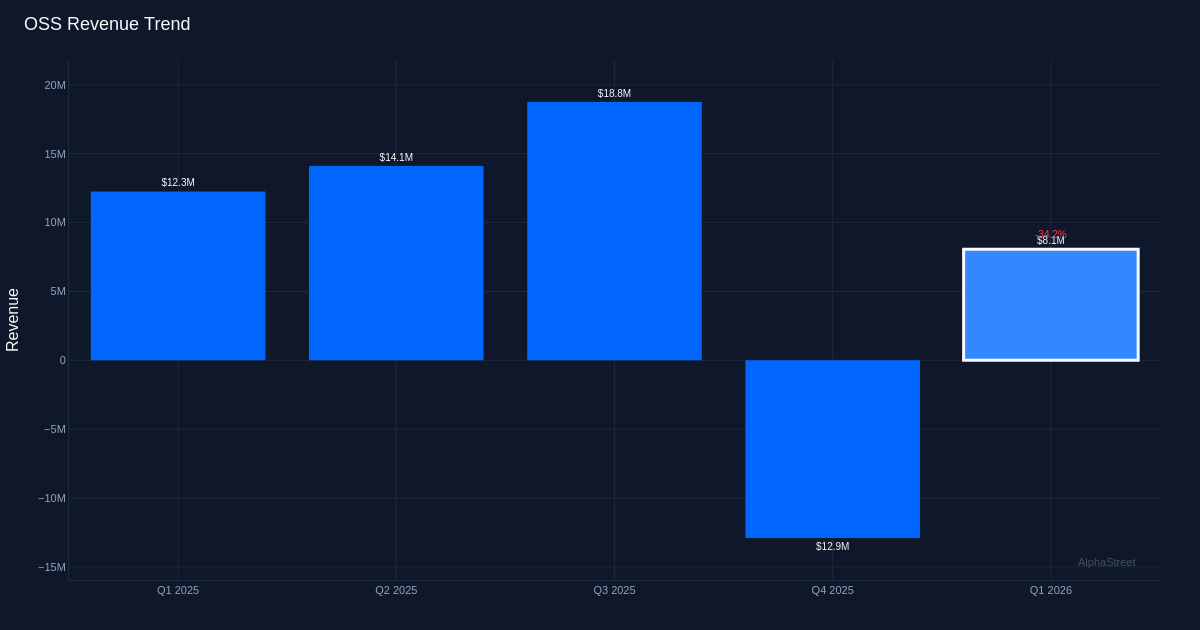

One Stop Systems (OSS) delivered a turnaround in Q1 2026, posting adjusted earnings of $0.01 per share versus analyst expectations of a $0.05 loss—a 120% beat that marked a sharp reversal from the $0.07 loss recorded a year earlier. The performance, driven by a 55% year-over-year revenue surge to $8.1 million and bolstered by $15 million in new bookings, sent shares soaring 56.9% to $15.33 as investors embraced the company’s improving operational trajectory and strengthening pipeline.

The quality of the earnings beat deserves scrutiny beyond the headline numbers. While revenue growth accelerated sharply, the company’s net margin remained negative at (-)6.4%, though it improved from Q1 2025. The gross margin of 51.5% demonstrates pricing power and favorable product mix, particularly important in the computer hardware space where component cost inflation has pressured peers. Operating margin of -8.3%, while still negative, reflects the company’s investment phase rather than structural unprofitability. The divergence between gross margin strength and operating losses points to fixed cost leverage as the key variable—as revenue scales, the path to sustained profitability appears clearer.

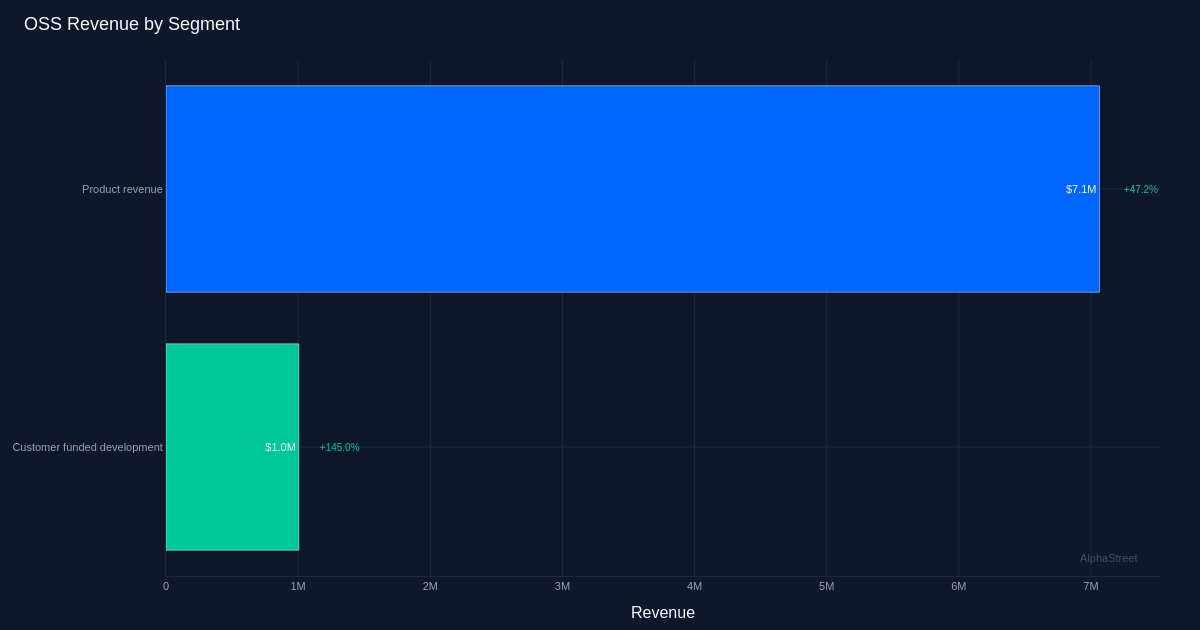

Segment performance reveals balanced strength across the business model. Product revenue of $7.1 million grew 47.2% year-over-year, representing the core commercial engine and accounting for 88% of total revenue. Customer-funded development revenue of $1.0 million surged 145%, indicating deepening relationships with strategic customers willing to fund custom solutions—a high-margin, sticky revenue stream that often converts to larger production orders. The outsized growth in customer-funded development suggests design wins that could materialize into significant production volume in coming quarters, though the timing remains uncertain given the project-based nature of this segment.

The forward-looking indicators matter more than the backward-looking results. The book-to-bill ratio of 1.8 and bookings of $15 million in a quarter that generated $8.1 million in revenue signal accelerating momentum. Management emphasized this point: “During the quarter, we generated nearly $15 million in new bookings that we expect to deliver in 2026 and 2027.” This backlog conversion timeline suggests revenue recognition spread across six quarters, implying a quarterly run-rate of $2.5 million from these bookings alone—before considering additional new orders. Management highlighted specific program visibility, noting “We expect this program to generate approximately $2 million in orders in 2026 with a five year opportunity in the range of an aggregate 10 million to $15 million.” The company’s confidence in 20-30% growth rates appears grounded in tangible pipeline rather than aspiration, with management commentary suggesting “that’s leading us to have that as we move through the factored elements of that is what’s continuing to strengthen our positive feeling about the ability to grow at that 20 to 30% range.”

Supply chain constraints emerge as the primary governor on upside potential. An analyst observation during the call crystallized the opportunity cost: “It sounds like if there were not the supply chain issues, there’s a chance you, you could have actually bumped up your outlook for 2026.” Component availability rather than demand appears to be the binding constraint, suggesting that as supply chains normalize, the company could accelerate revenue conversion from its expanding backlog. This dynamic is particularly relevant in specialized computer hardware where long lead-time components like custom processors or military-grade parts can delay entire system deliveries.

Operating cash flow of $4.0 million in the quarter—representing 49% of revenue—provides financial flexibility unusual for a company at this revenue scale. This cash generation, combined with positive net income and growing bookings, positions the company to self-fund growth without dilutive capital raises. The cash flow strength suggests efficient working capital management and favorable payment terms with customers, critical factors for a hardware company navigating component procurement challenges.

The 56.9% stock surge reflects investor enthusiasm for the inflection from consistent losses to profitability, but the $15.33 price must be evaluated against execution risk. At this level, the market is pricing in successful conversion of the $15 million backlog and continued bookings momentum. The valuation appears to discount material risk of supply chain disruption or program delays, common hazards in defense and specialized computing contracts.

What to Watch: Q2 2026 results will clarify whether the book-to-bill strength translates to sustained revenue growth or if supply chain constraints delay backlog conversion. Monitor gross margin trajectory—maintaining the 51.5% level while scaling volume would validate pricing power and favorable mix. Track customer-funded development conversion to production orders, as this represents the highest-quality revenue pipeline. Any guidance updates on the $10-15 million five-year program opportunity and progress toward the 20-30% annual growth target will signal management’s confidence in sustaining the inflection.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.

[ad_2]

Source link