[ad_1]

AlphaStreet Newsdesk powered by AlphaStreet Intelligence

Q2 EPS guidance — adjusted $0.19 – $0.21|Stock $10.04 (-2.5%)

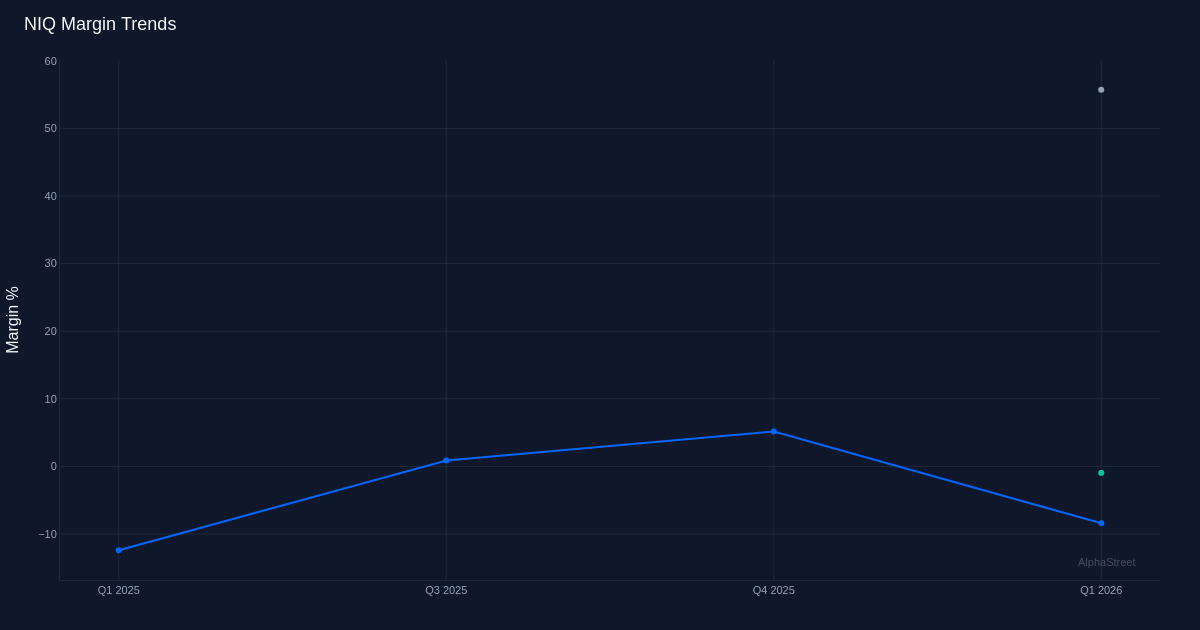

EPS YoY +130.6%|Rev YoY +11.1%|Net Margin -8.4%

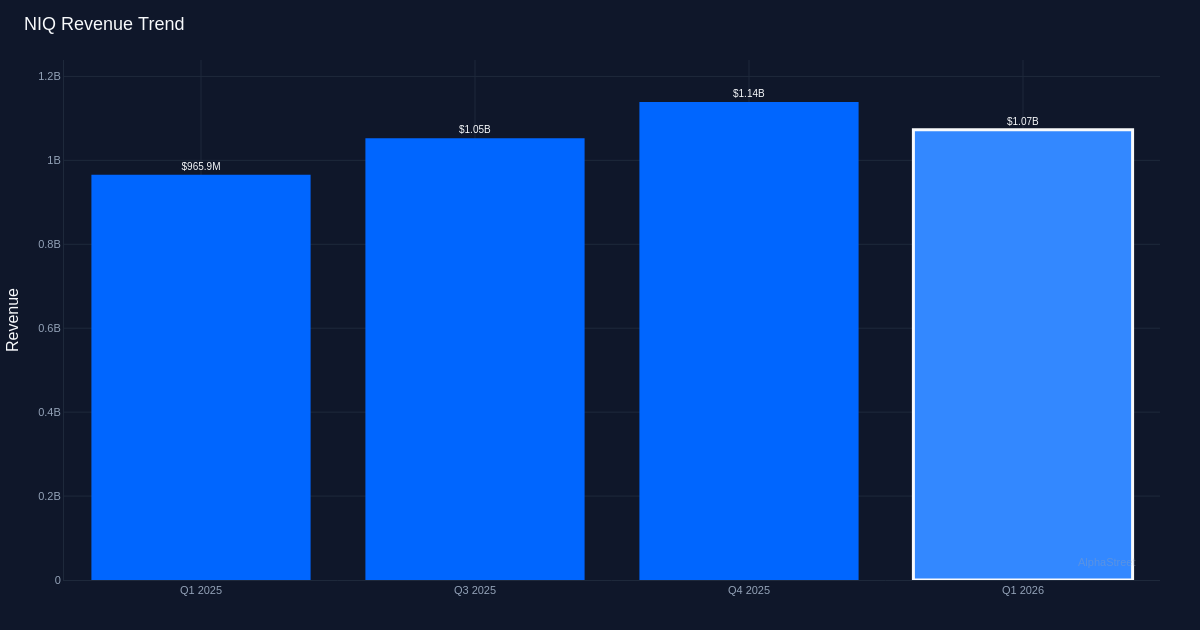

NIQ Global Intelligence (NIQ) delivered a commanding Q1 beat, crushing expectations by 50% with adjusted EPS of $0.15 against the $0.10 consensus. The data analytics firm’s $1.07 billion revenue performance exceeded guidance while demonstrating meaningful margin expansion, suggesting operational leverage is finally materializing after the company’s post-IPO transformation. Yet investors sent shares down 2.5% to $10.04, likely reflecting concern that the quarter’s momentum—management admits Q1 is “traditionally our lowest quarter”—may already be priced in or skepticism about the sustainability of margin gains.

The earnings quality story here is unambiguous: this was expansion-driven, not cost-cutting theater. Gross margin held firm at 55.9%, while adjusted EBITDA surged 19.1% year-over-year to $224.8 million. Management noted that “adjusted EBITDA growth accelerated to 19.1% year over year to $224.8 million with margins expanding 150 basis points year over year to 21%.” That 150 basis point expansion is the critical detail—revenue grew 11.1% on a reported basis, but profitability grew nearly twice as fast. Net margin improved 4.0 percentage points year-over-year from negative 12.4% to negative 8.4%, still underwater but moving in the right direction. Operating margin remains challenged at negative 1.0%, though operating income of $10.2 million represents a significant improvement from year-ago levels when the company posted an adjusted loss per share of $0.49.

Organic constant currency growth of 5.1% strips away the acquisition and FX tailwinds, revealing the true underlying demand picture. The gap between reported 11.1% growth and organic 5.1% growth indicates M&A and currency contributed roughly 600 basis points, meaning more than half the headline growth came from inorganic sources. This isn’t necessarily problematic if integrations are proceeding smoothly, but it does mean investors should temper expectations that double-digit growth is the new baseline. The subscription revenue metric provides additional confidence: annualized subscription revenue reached $2.93 billion, with management highlighting that “Q1 net dollar retention was 104%, gross retention was 99% and annualized subscription revenue was $2.9 billion up 5.9%.” A 104% net dollar retention rate demonstrates existing customers are expanding their spending, while 99% gross retention suggests minimal churn—both critical indicators of product-market fit in a subscription business model.

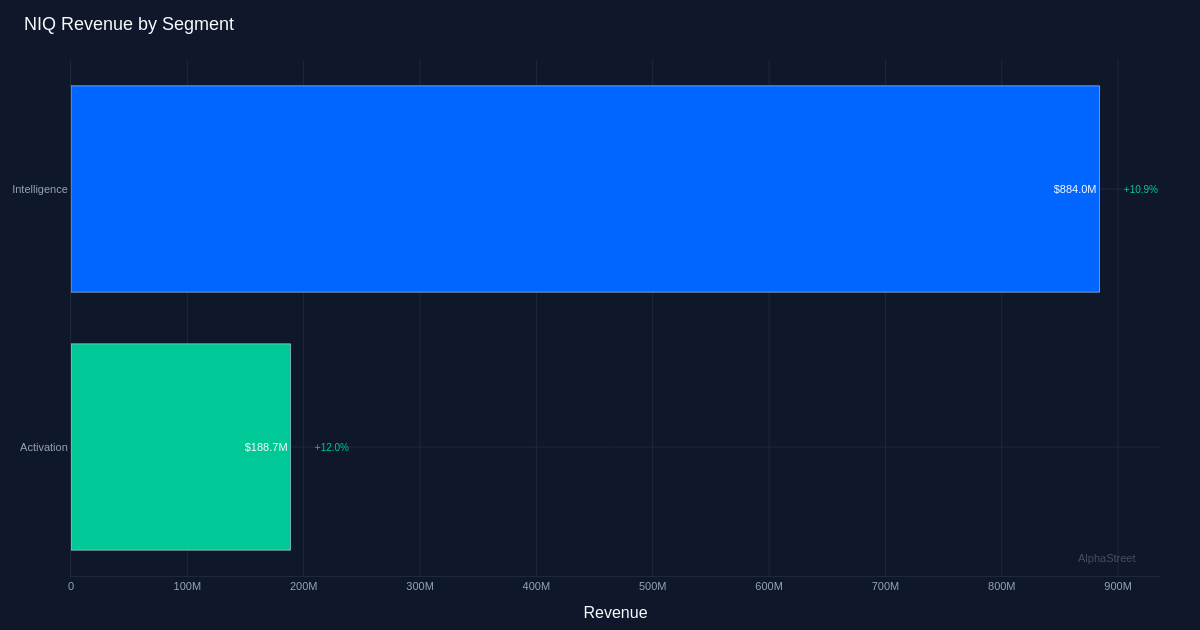

Segment performance showed balanced strength with Activation slightly outpacing Intelligence. The Intelligence segment generated $884.0 million with 10.9% growth, representing the bulk of revenue at roughly 83% of the total. Activation contributed $188.7 million growing 12.0% year-over-year, a modest acceleration compared to the core Intelligence business. The Activation segment’s faster growth rate, despite its smaller base, suggests NIQ’s efforts to expand beyond traditional intelligence offerings into more execution-oriented solutions may be gaining traction. However, the narrow growth differential—just 110 basis points—indicates this isn’t yet a meaningful driver of portfolio mix shift.

Guidance for Q2 sets up another beat while implying sequential acceleration. Management’s $0.19 to $0.21 EPS range (midpoint $0.20) would represent the second-highest quarterly performance in the trailing four quarters, exceeded only by Q4 2025’s $0.20. Revenue guidance of $1.10 billion to $1.11 billion at the midpoint would mark 2.8% sequential growth from Q1—consistent with management’s assertion that Q1 is the seasonal low point. The midpoint would also represent roughly 13-14% year-over-year growth assuming similar growth rates to Q1, suggesting the company expects to sustain or slightly accelerate its reported growth trajectory. Management delivered on Q1 expectations by noting revenue “exceeding the top end of our guidance and in line with consensus,” establishing credibility for the Q2 outlook.

The muted stock reaction despite a substantial earnings beat suggests investors are either discounting Q1 as seasonally weak or remain concerned about the path to sustained profitability. Trading at $10.04 after a 2.5% decline, the market appears to be waiting for proof that margin expansion can continue while maintaining growth. The negative operating margin and net margin, despite improvement, remind investors that NIQ remains in a prove-it phase.

What to Watch: Track whether the April revenue strength management referenced translates to Q2 guidance achievement or another beat. Monitor net dollar retention sustainability above 100%—any decline below that threshold would signal customer spending contraction. The spread between reported and organic constant currency growth deserves attention; if inorganic contributions continue exceeding organic by 2:1, question whether the growth profile is sustainable post-integration.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.

[ad_2]

Source link