[ad_1]

AlphaStreet Newsdesk powered by AlphaStreet Intelligence

Guidance adjusted $1.26 – $1.30|Stock $40.00 (-0.1%)

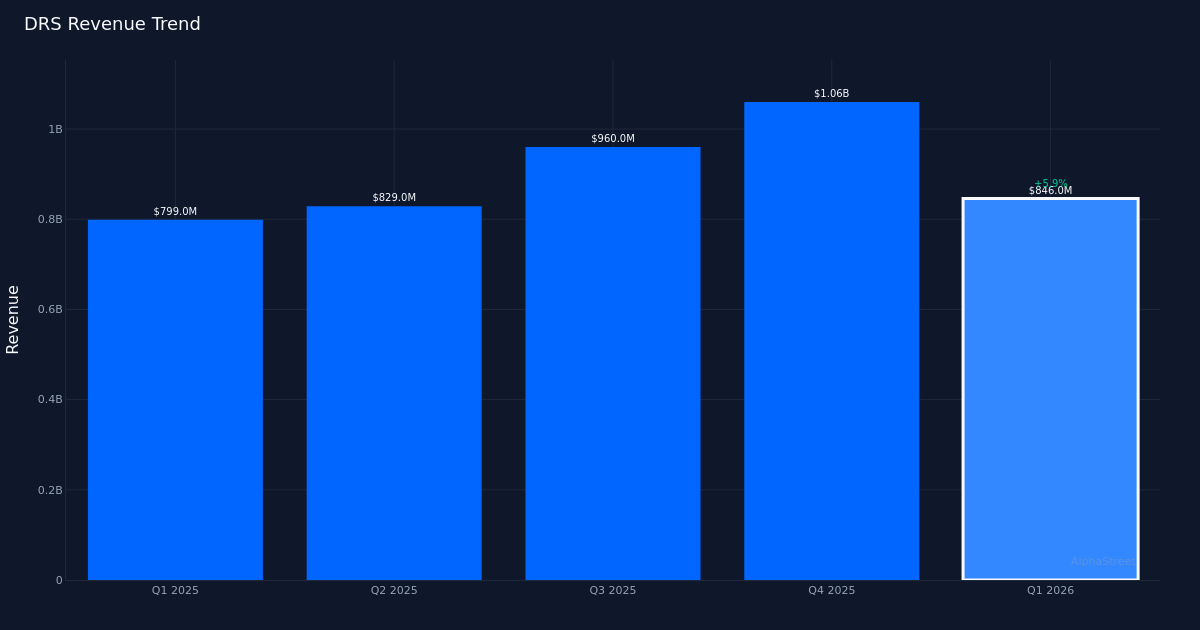

Solid Beat. Leonardo DRS, Inc. (NASDAQ:DRS) delivered Q1 2026 adjusted earnings of $0.26 per share, surpassing the $0.21 consensus by 30.0%. The aerospace and defense contractor generated $846.0M in revenue for the quarter, representing a 6.0% increase from the $799.0M recorded in Q1 2025. Net income reached $69.0M as the company continued executing on its defense modernization programs. The stock traded largely unchanged following the report, suggesting investors may have anticipated the strong performance or are waiting for additional clarity on the sustainability of growth momentum.

Revenue-Driven Performance. The quality of this earnings beat appears fundamentally sound, driven by top-line expansion rather than aggressive cost management alone. The 6.0% year-over-year revenue growth demonstrates genuine business momentum in an environment where defense budgets remain robust. With net income of $69.0M supporting the adjusted earnings figure, the company appears to be converting revenue growth into bottom-line profitability organically. This revenue-driven beat carries more weight than one manufactured through temporary expense reductions, particularly in the capital-intensive aerospace and defense sector where sustained program execution matters most.

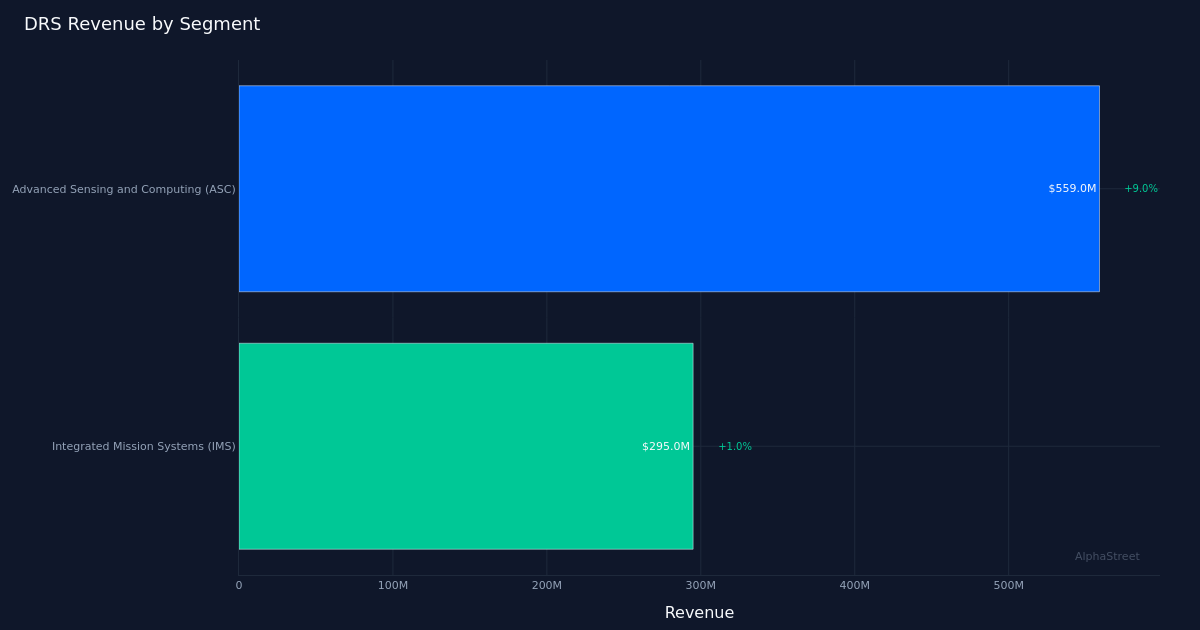

Sensing Segment Strength. Advanced Sensing and Computing (ASC) led the portfolio with $559.0M in revenue, up 9.0% year-over-year. This segment’s outperformance relative to the company’s overall 6.0% revenue growth indicates strong demand for Leonardo DRS’s sensing and computing capabilities, which serve critical defense applications. The ASC division’s momentum reflects broader Pentagon priorities around electronic warfare, intelligence gathering, and battlefield awareness systems. Funded backlog stood at $4.70B for the quarter, providing substantial revenue visibility and underscoring the company’s competitive positioning in key defense programs.

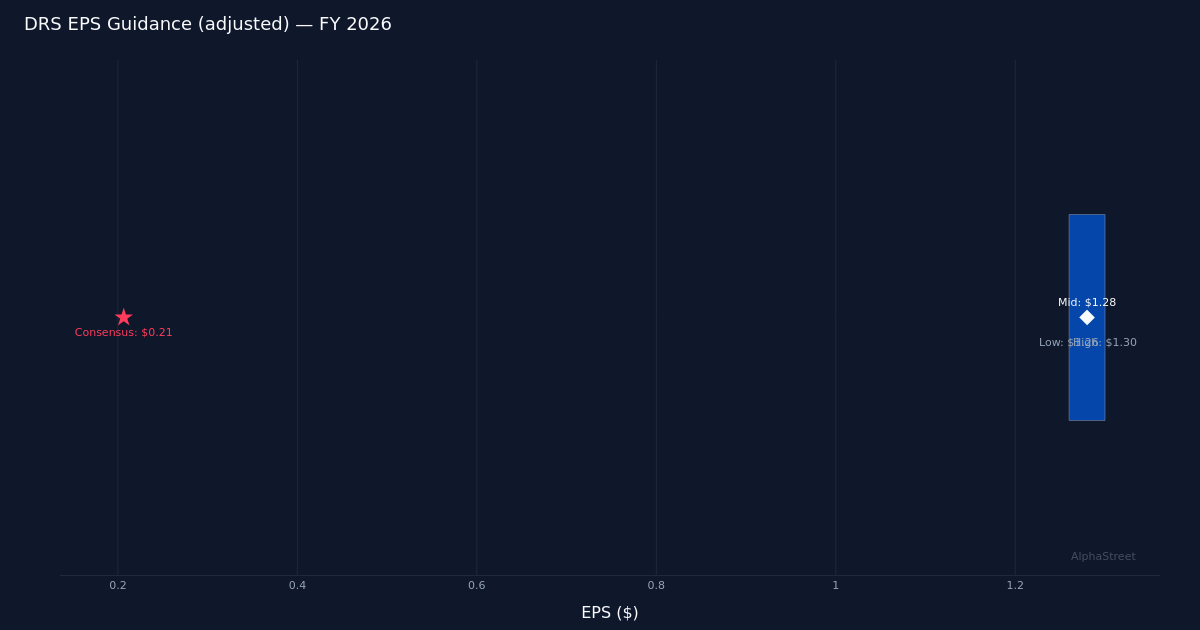

Full-Year Outlook. Management expects FY 2026 adjusted EPS of $1.26 to $1.30, establishing a clear roadmap for investors to assess execution through the remainder of the year. The midpoint of $1.28 implies meaningful earnings growth as the company scales production and delivers on its contract commitments. This guidance framework suggests management confidence in converting the company’s substantial backlog into financial results, though investors will monitor program execution risk and supply chain stability as potential variables that could influence achievement of these targets.

Analyst Positioning. Wall Street maintains a constructive stance on Leonardo DRS, with analyst consensus standing at 7 buy ratings, 3 hold ratings, and 0 sell ratings. This tilt toward bullish recommendations reflects recognition of the company’s exposure to defense modernization spending and its specialized technology portfolio. The absence of sell ratings indicates few concerns about fundamental deterioration, while the presence of hold ratings suggests some analysts may be calibrating expectations around valuation or awaiting additional proof points on margin expansion.

What to Watch: Monitor whether Leonardo DRS can sustain the 9.0% growth rate demonstrated in Advanced Sensing and Computing across subsequent quarters, and whether the $4.70B funded backlog translates into accelerating revenue conversion as production ramps on key platforms.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.

[ad_2]

Source link