[ad_1]

CarMax, Inc. (NYSE: KMX ) witnessed a sales boom during the pandemic as people opted for existing cars rather than spending larger sums on new vehicles, due to economic uncertainty. But the company’s recent performance suggests that weak buyer sentiment amid fears of a recession and looming inflationary pressures is weighing on demand for used cars.

Management has a recovery plan, with a focus on cutting costs, implementing a new sales mix, and gaining capital flexibility by pausing share buybacks and delaying planned store openings. CarMax posted the best stock market performance in the COVID era, especially in the early stages of the crisis. However, the trend reversed in the second half of 2021 – after stocks rose to all-time highs. KMX entered a downward spiral since then and has lost most of its gains.

Outlook

The outlook of experts shows that as the company enters the new fiscal year, the stock has more risks than upside risks. Shareholders shouldn’t get too excited about yields as prices are set to drop again this year. Ideally, prospective buyers should wait patiently until they see a good entry point. Those who already own shares can continue to hold as this is not the right time to sell.

Continued pressure on consumer spending, due to high inflation and rising interest rates, will likely deter people from splurging on big items like cars in the future. That means it will take some time for CarMax’s sales and profits to recover.

Q4 is weak on the Cards

When the company reports its fourth-quarter results on April 11, before regular trading begins, markets will be looking for updates on emerging trends in the industry. Meanwhile, market watchers are cautious about the outlook, predicting a 76% plunge in earnings to $0.24 per share. It expects revenue to fall 21% year over year to $6.05 billion in the three months ending February 2023.

CarMax CEO Bill Nash said on the Q3 earnings call: “Actions taken during the quarter included reducing SG&A, selling an older, lower-priced vehicle mix, slowing purchases due to a steep market decline, maintaining serviceable inventory units while driving total inventory dollars more than 25% year-over-year, raising rates consumer CAFs to help offset the increase in cost of funds, pause share buyback to give us capital flexibility, and slow store growth we plan for the next fiscal year for five locations while maintaining our ability to open more locations if market conditions change.”

Sales under Pressure

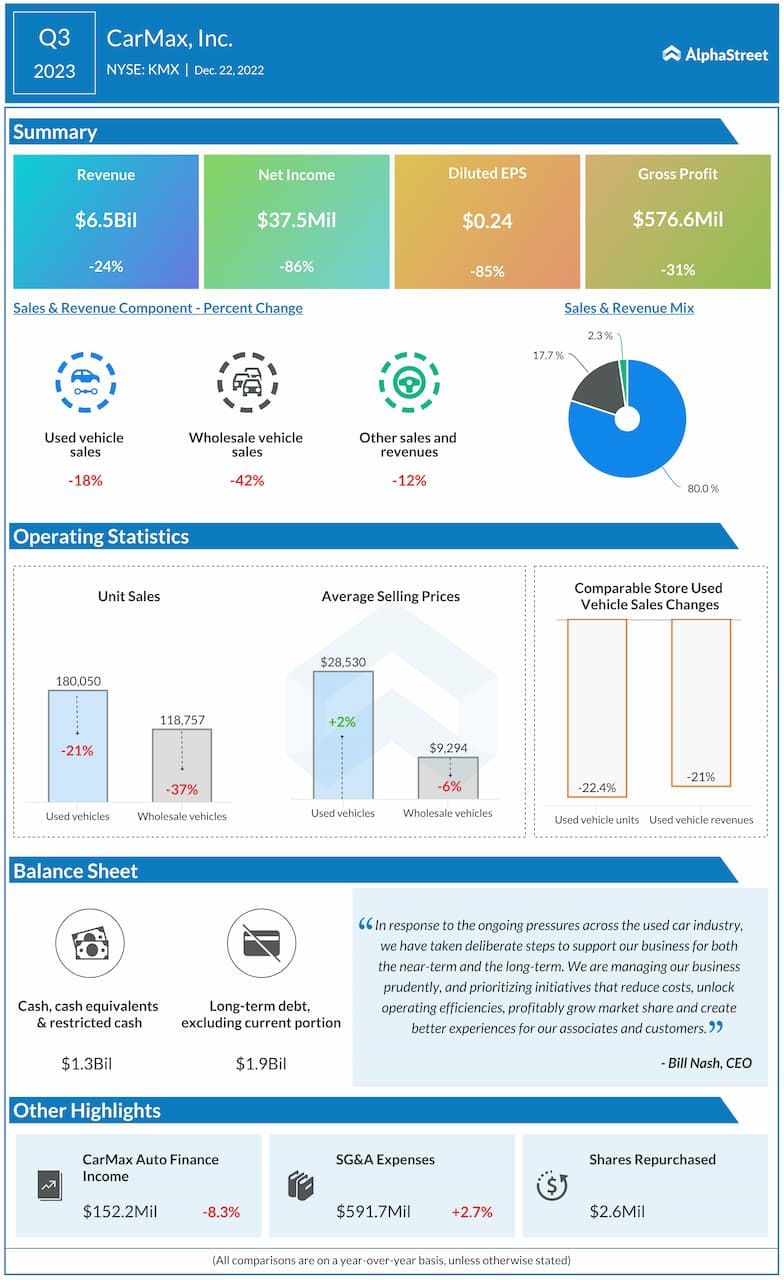

The forecast is in line with the company’s disappointing performance in recent quarters, marked by declining earnings and inconsistent revenue performance. In the third quarter, earnings declined and missed consensus estimates for the fourth time in a row. The weak underlying performance was due to a 24% decline in revenue to $6.5 billion, which was also unexpected. All three operating segments contracted, which was almost identical to the performance of the previous quarter. Same-store used unit sales fell 22.4%, and total retail used units sold fell 20.8%.

The stock has declined 37% in the past twelve months. Meanwhile, stocks traded slightly higher on Monday – extending a recent trend – in a sign that they may be gaining momentum ahead of earnings.

[ad_2]

Source link