[ad_1]

AlphaStreet Newsdesk powered by AlphaStreet Intelligence

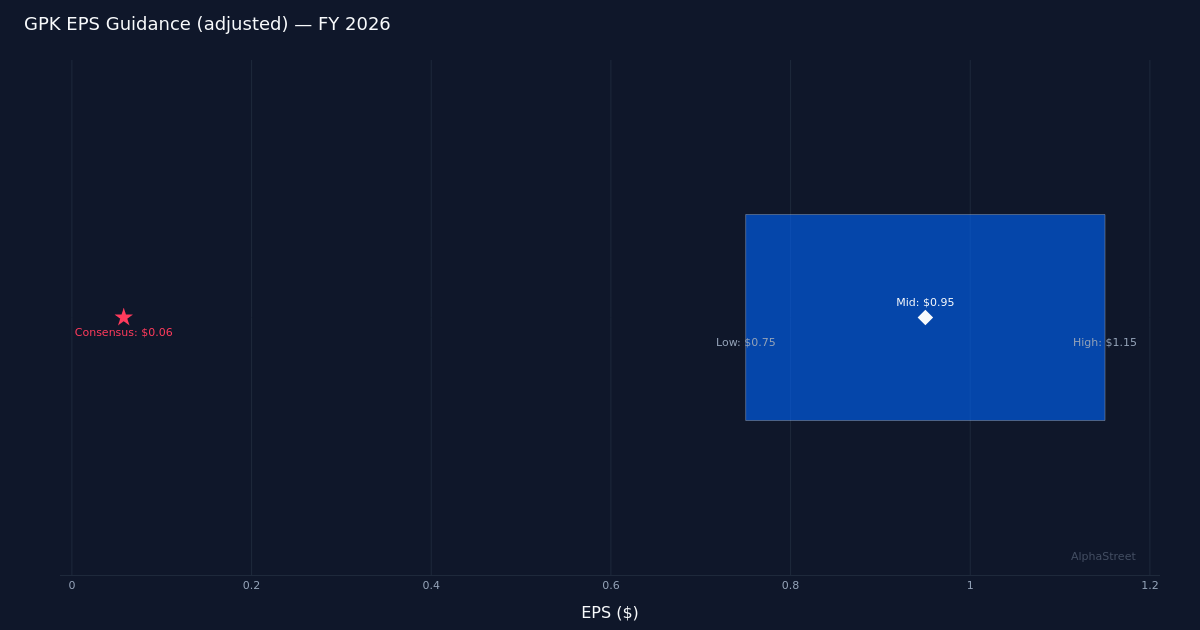

Guidance adjusted $0.75 – $1.15|Stock $9.56 (-1.4%)

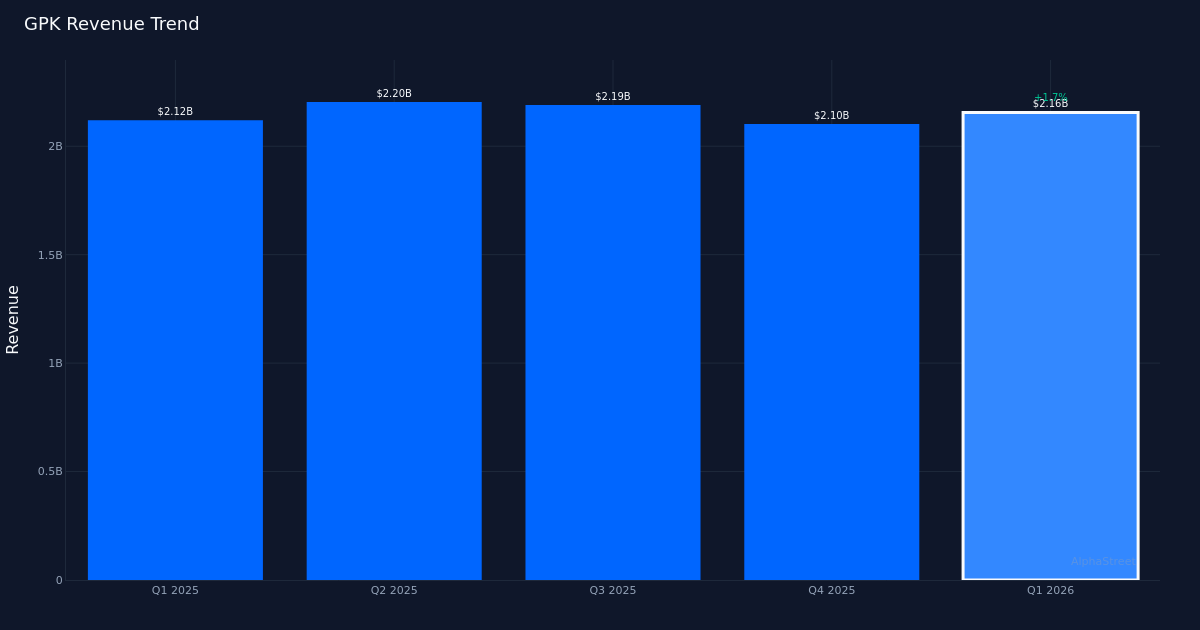

Solid Beat. Graphic Packaging Holding Company (NYSE:GPK) delivered a strong Q1 2026 performance, posting adjusted EPS of $0.09 that handily topped Wall Street’s $0.06 estimate, representing a beat by 50.0%. The company generated $2.16B in revenue for the quarter, up 2.0% from $2.12B in Q1 2025, demonstrating modest but steady topline momentum in what remains a challenging environment for packaging manufacturers. Bottom-line profit came in at $28.0M as the company balanced pricing discipline with operational efficiency.

Volume Recovery. The quality of this beat appears encouraging, driven in part by fundamental demand improvement rather than purely financial engineering. Volumes rose 1.0% for the quarter, a positive signal that suggests underlying customer demand is stabilizing after a period of destocking and consumer softness. This volume growth, combined with revenue expansion, indicates the company is successfully navigating the shift toward sustainable packaging solutions while maintaining market share in core categories like paperboard-based consumer packaging.

Wide Guidance Range. Management provided FY 2026 guidance that reveals significant uncertainty about the year ahead. The company projected adjusted EPS in the $0.75 to $1.15 range, an unusually wide spread that suggests management is grappling with volatile input costs, currency fluctuations, or customer ordering patterns. Revenue guidance for FY 2026 was set at $8.40B to $8.60B, implying modest growth at the midpoint relative to the current quarterly run rate. The breadth of these ranges will likely concern investors seeking greater visibility into second-half performance.

Muted Market Response. Despite the substantial earnings beat, shares traded at $9.56, down 1.4%, suggesting investors remain cautious about the stock’s near-term prospects. This negative reaction likely reflects concerns about the wide guidance range, competitive pressures in commodity packaging markets, or broader sector headwinds as consumer packaged goods companies manage inventory levels conservatively. The disconnect between strong quarterly execution and stock performance highlights the market’s focus on future growth trajectory rather than backward-looking results.

Analyst Skepticism. Wall Street sentiment remains decidedly lukewarm, with consensus standing at just 1 buy rating against 12 hold and 5 sell recommendations. This overwhelmingly neutral-to-negative stance suggests analysts question whether recent operational improvements can translate into sustained margin expansion and cash generation, particularly as the company navigates capital-intensive investments in sustainable packaging infrastructure while facing potential pricing pressure from larger competitors.

What to Watch: Management’s ability to narrow the wide FY 2026 guidance range and sustain positive volume momentum will be critical. Investors should monitor whether pricing discipline holds as input costs fluctuate and whether the volume recovery proves durable or merely reflects temporary customer restocking.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.

[ad_2]

Source link