[ad_1]

AlphaStreet Newsdesk powered by AlphaStreet Intelligence

Stock $41.49 (-1.6%)

EPS YoY +24.6%|Rev YoY -7.6%|Net Margin 14.7%

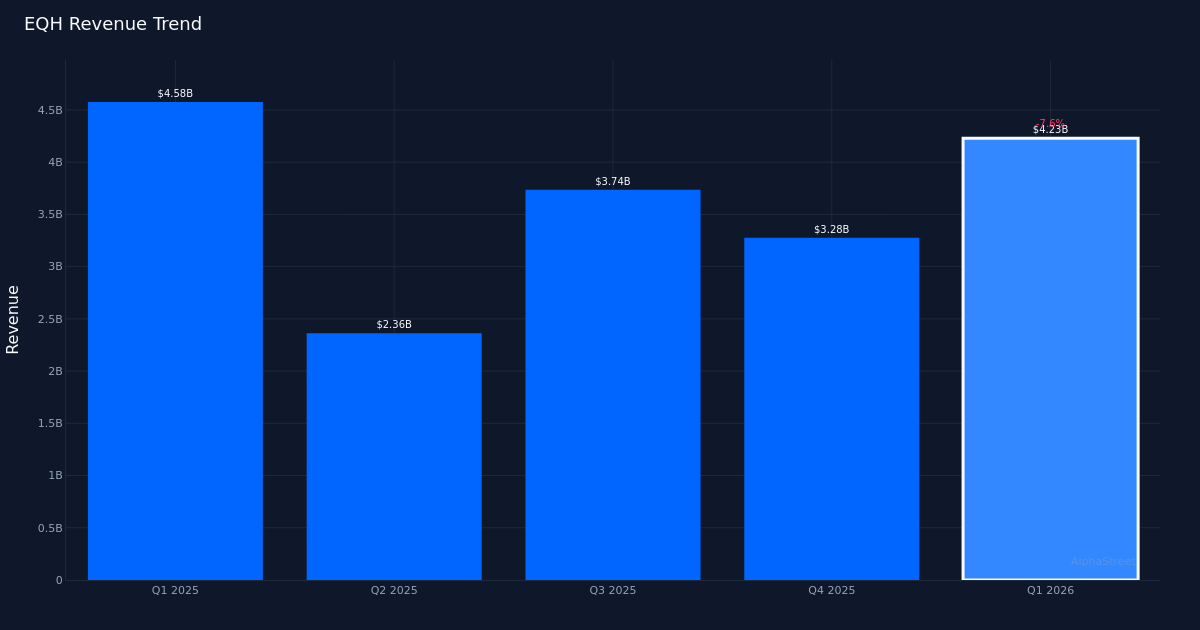

Equitable Holdings (EQH) barely missed analyst expectations in Q1 2026, but the headline disappointment masks a story of exceptional profitability improvement and business mix evolution. The financial services firm reported adjusted EPS of $1.62, a penny short of the $1.63 consensus estimate—a 0.6% miss that triggered a modest 1.6% stock decline to $41.49. Yet beneath the surface-level miss lies a 24.6% year-over-year earnings surge driven by dramatic margin expansion, even as the company navigated a challenging revenue environment.

The earnings quality tells a far more compelling story than the top-line miss suggests. Net margin expanded year-over-year to 14.7% in the current quarter. This improvement is particularly striking given that revenue declined 7.6% to $4.23B from $4.58B in the prior-year period. Adjusted net income surged to $472.0M from $421.0M, demonstrating that management has successfully pivoted from volume-driven growth to profitability optimization. This isn’t cost-cutting for survival—it’s strategic repositioning toward higher-margin business lines. The Wealth Management segment exemplifies this shift, with management noting that the division “delivered another strong growth quarter with $2 billion of advisory net inflows over the last 12 months,” pointing to sustainable fee-based revenue momentum that typically carries superior economics compared to transaction-driven income.

The four-quarter revenue trajectory reveals significant quarter-to-quarter volatility that complicates trend analysis. Sequential revenue progression shows Q2 2025 at $2.36B, Q3 2025 at $1.45B, Q4 2025 at $3.28B, and Q1 2026 at $4.23B—a pattern that defies simple characterization as either acceleration or deceleration. The current quarter’s $4.23B represents a substantial sequential increase from Q4’s $3.28B, yet remains below the Q1 2025 baseline of $4.58B. This volatility likely reflects the episodic nature of certain revenue streams in asset management and retirement services, where market conditions, client activity levels, and investment performance fees can create lumpiness.

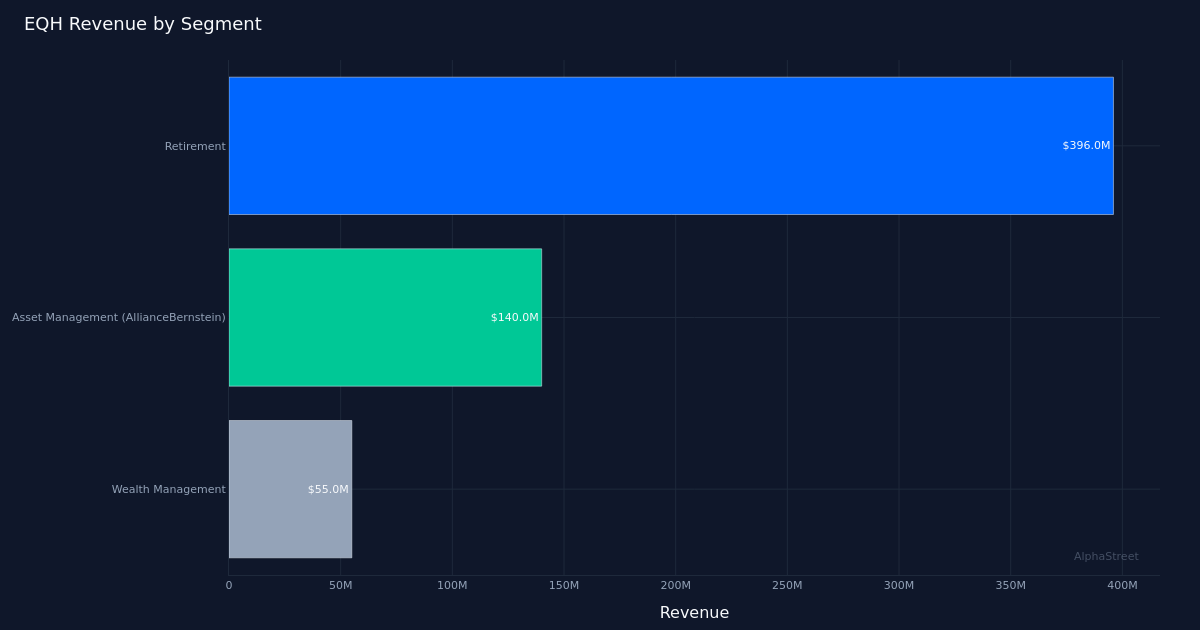

Segment performance reveals a well-diversified profit engine with Retirement Services remaining the dominant contributor. The Retirement segment generated $396.0M in the quarter, representing roughly 64% of total net income and underscoring the business’s foundation in stable, recurring revenue streams. AllianceBernstein’s Asset Management segment contributed $140.0M, while Wealth Management added $55.0M. The AllianceBernstein platform appears positioned for accelerated growth, with management highlighting that “total private markets AUM increased 13% year over year to $85 billion and AB remains on track to meet or exceed its target of 90 to 100 billion in AUM by the end of 2027.” This private markets focus is strategically astute, as alternative investments typically command higher fees and stickier client relationships than traditional equity and fixed income mandates. Management’s confidence in achieving the 2027 AUM target suggests momentum in client acquisition and product development.

Management’s 2026 guidance projects continued outperformance despite the quarterly miss. The company reiterated that it expects “earnings per share growth to exceed the high end of our 12 to 15% target range in 2026,” implying full-year EPS growth above 15% from 2025 levels. Given that Q1 already delivered 24.6% year-over-year EPS growth, this guidance appears conservative unless management anticipates significant headwinds in subsequent quarters. The commitment to exceed the high end of the range, rather than simply meet it, signals management’s conviction in the business trajectory. This confidence likely stems from the combination of margin expansion initiatives already bearing fruit and organic growth momentum, particularly in higher-margin advisory businesses where “Rylas up 14% and 1.3 billion of net flows translating to a 6% trailing 12 month organic growth rate” demonstrates robust client demand.

The analyst community maintains uniformly bullish sentiment despite the miss, suggesting expectations for continued execution. Recent ratings from Mizuho, Keefe Bruyette & Woods, Wells Fargo, UBS, and Evercore ISI Group all carry Outperform, Buy, or Overweight recommendations issued within days of the earnings release. This consensus view reflects confidence that the quarterly miss represents noise rather than a fundamental deterioration. The 0% beat rate over the last quarter (having missed this one) raises questions about whether guidance-setting needs recalibration, but the stock’s modest 1.6% decline suggests investors are looking past the near-term shortfall toward the margin expansion story and guidance affirmation.

The retirement spread income business showed sequential momentum that could drive upside in coming quarters. Management noted that “quarter over quarter spread income NIM was up 11 million quarter over quarter,” indicating that the core retirement annuity business is benefiting from favorable interest rate dynamics or improved asset-liability management. This $11 million sequential improvement may seem modest relative to total net income of $621.0M, but spread income represents highly predictable, capital-light earnings that warrant premium valuation multiples. As this metric continues improving, it should provide a stable earnings foundation that allows the company to invest more aggressively in growth initiatives within Wealth Management and private markets.

The $41.49 stock price reaction reflects investor uncertainty about whether margin gains can offset revenue pressure. The 1.6% post-earnings decline suggests the market is weighing impressive profitability improvements against concerns about top-line momentum. Without 52-week range context, the magnitude of this move is difficult to interpret, but the muted response—neither panic selling nor enthusiasm—indicates investors are adopting a wait-and-see posture. The key question is whether management can reignite revenue growth while maintaining or expanding the 14.7% net margin achieved this quarter. If subsequent quarters demonstrate that Q1’s revenue level of $4.23B represents a new baseline rather than a peak, the current valuation could prove attractive given the earnings growth guidance.

What to Watch: Q2 revenue trajectory will be critical to assess whether the sequential improvement from $3.28B to $4.23B represents sustainable momentum or quarter-end timing effects. AllianceBernstein’s progress toward the $90-100 billion private markets AUM target by end-2027 will signal whether the higher-margin growth strategy is on track. Wealth Management advisory net flows beyond the $2 billion trailing-twelve-month figure will indicate if the firm can sustain organic growth in its highest-quality revenue stream. Finally, spread income margin progression in Retirement Services will reveal whether the $11 million sequential improvement represents the beginning of a sustained uptrend or merely quarterly noise in a stable business line.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.

[ad_2]

Source link