[ad_1]

AlphaStreet Newsdesk powered by AlphaStreet Intelligence

Stock $140.68 (+2.5%)

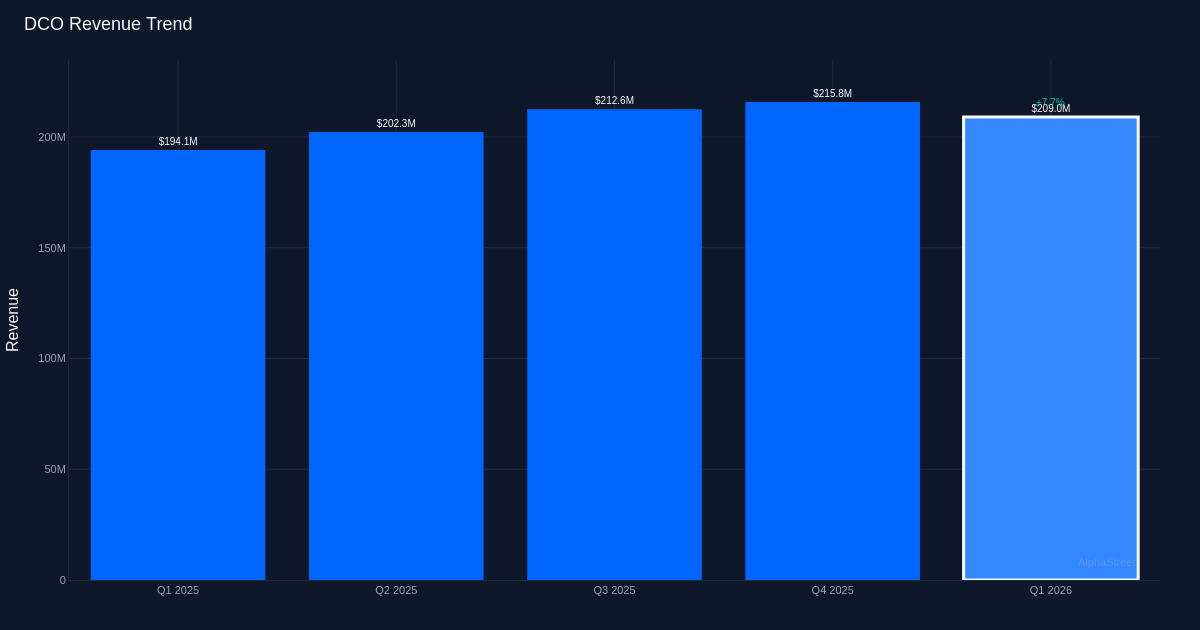

Earnings Miss. Ducommun Incorporated (NYSE: DCO) reported Q1 2026 adjusted diluted EPS of $0.75 per share, falling short of the $0.79 consensus estimate by 5.1%. The aerospace and defense manufacturer generated $209.0M in revenue for the quarter, representing 9.0% growth from $192.5M in Q1 2025. Adjusted net income reached $11.7M for the quarter, while the company maintained an adjusted EBITDA margin of 16.9%. Despite the bottom-line shortfall, shares traded up 2.5% to $140.68, suggesting investors found encouragement in the top-line momentum and operational performance.

Revenue-Driven Growth. The earnings miss appears less concerning when examined through the lens of quality—this was a revenue-driven quarter with solid year-over-year expansion rather than a margin compression story. The 9.0% top-line growth demonstrates healthy underlying demand across Ducommun’s aerospace and defense portfolio, a critical distinction for investors evaluating the sustainability of the business trajectory. The company’s adjusted EBITDA margin of 16.9% reflects operational discipline in a period of continued investment, particularly noteworthy given the challenging aerospace supply chain environment that has pressured peers throughout the sector.

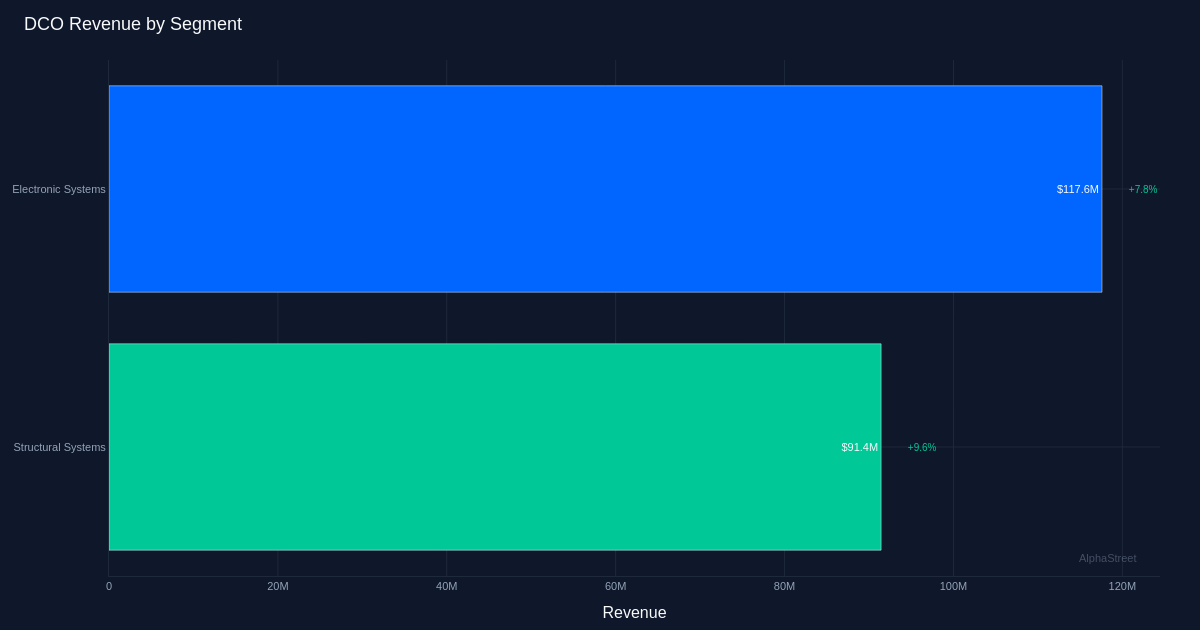

Electronic Systems Strength. Electronic Systems led performance with $117.6M in revenue, up 7.8% year-over-year, underscoring the segment’s role as the company’s growth engine. This division’s resilience speaks to Ducommun’s exposure to high-value electronic and structural systems across both commercial aerospace and defense platforms. The segment’s performance is particularly relevant given ongoing defense modernization programs and the continued recovery in commercial aviation production rates, both of which should provide multi-year tailwinds for specialized suppliers like Ducommun.

Backlog Visibility. The company maintained $1.07 billion remaining performance obligations on a consolidated basis at quarter-end, providing substantial revenue visibility as management works through its order book. This backlog figure serves as a key indicator of near-to-medium term revenue potential and reflects the long-cycle nature of aerospace and defense contracting. For institutional investors, this metric offers confidence in the durability of Ducommun’s growth trajectory independent of near-term macroeconomic volatility.

Analyst Sentiment. Wall Street maintains a constructive view with consensus ratings of 6 buy, 1 hold, and 0 sell, suggesting the Street sees through the modest earnings miss to focus on the company’s strategic positioning and growth prospects. The positive stock reaction following results indicates the market shares this assessment, viewing the quarter as a validation of operational momentum rather than a fundamental concern.

What to Watch: Monitor how Ducommun converts its substantial backlog into revenue and margin expansion through the remainder of 2026. The company’s ability to execute on its Electronic Systems pipeline while maintaining EBITDA margins above the mid-teens threshold will determine whether the current valuation multiple expands alongside the aerospace sector’s broader recovery.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.

[ad_2]

Source link