[ad_1]

AlphaStreet Newsdesk powered by AlphaStreet Intelligence

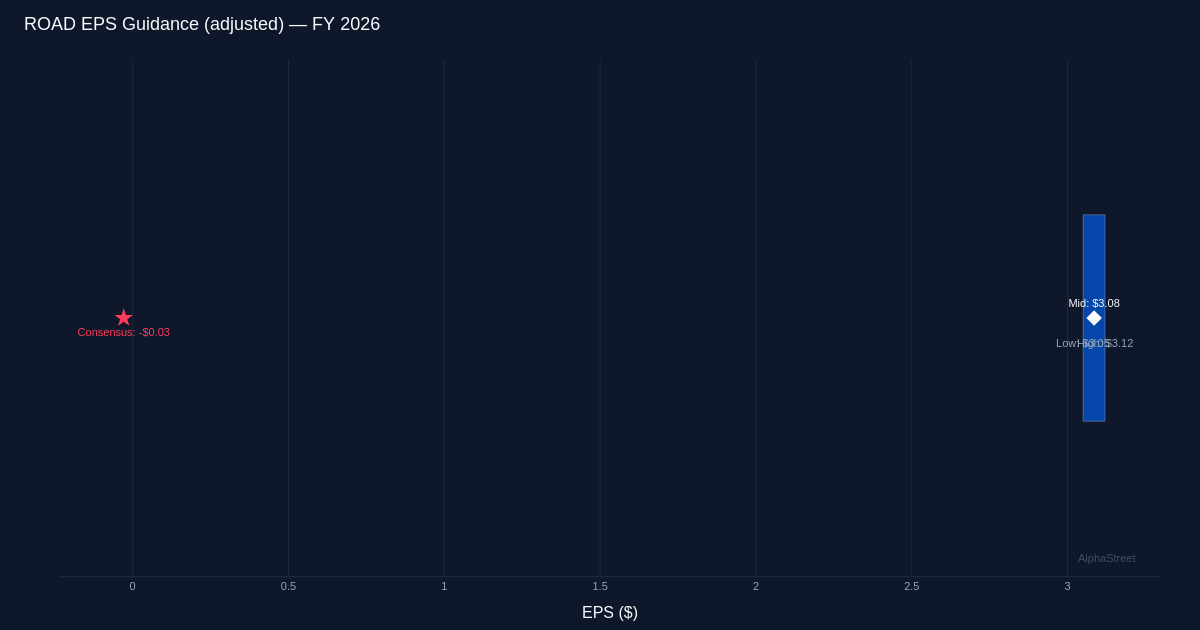

Guidance $3.59B – $3.65B|Stock $139.84 (+6.4%)

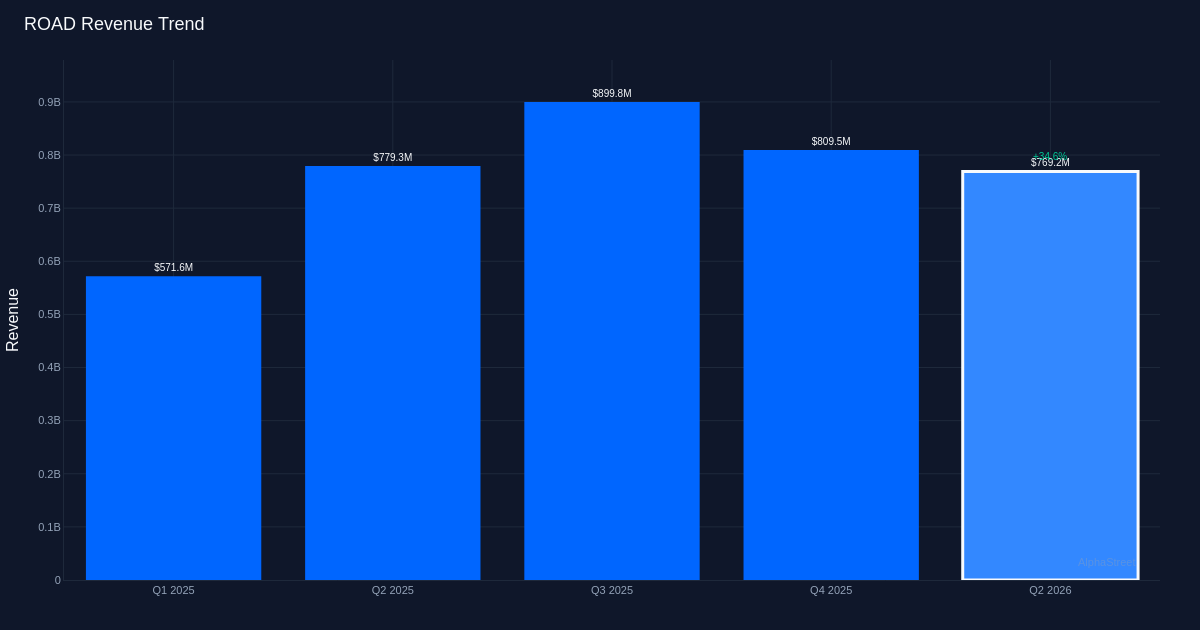

Decisive Beat. Construction Partners, Inc. (NASDAQ:ROAD) delivered a resounding Q2 2026 performance, reporting adjusted diluted earnings of $0.18 per share against a consensus estimate of -$0.03 per share, representing a beat by 700.0%. The company generated $769.2M in revenue for the quarter, up 34.5% from $571.7M in Q2 2025, demonstrating robust demand in its engineering and construction operations. Shares surged 6.4% to $139.84 following the release, reflecting investor enthusiasm for the stronger-than-expected results.

Revenue-Driven Expansion. The quality of this beat appears exceptionally strong, with top-line growth serving as the primary catalyst rather than purely cost optimization. Organic revenue growth of +11.0% for the quarter underscores genuine business momentum beyond acquisition contributions. Adjusted bottom-line profit came in at $10.4M, a meaningful improvement that suggests operational leverage is working in the company’s favor as revenue scales. The combination of substantial revenue expansion and positive earnings in a quarter where the Street had expected a loss signals genuine operational strength rather than financial engineering.

Robust Project Pipeline. Construction Partners reported a project backlog of $3.14B at quarter end, providing substantial visibility into future revenue streams and demonstrating continued success in securing new contracts. This backlog figure offers investors confidence that the company’s growth trajectory can be sustained as these awarded projects move into execution phases. The magnitude of committed work positions the business well for revenue conversion through the remainder of the fiscal year and beyond.

Confident Full-Year Outlook. Management issued FY 2026 guidance calling for revenue of $3.59B to $3.65B. This forward guidance suggests management expects the momentum demonstrated in Q2 to persist, with the midpoint of the revenue range implying continued strong year-over-year growth.

Analyst Sentiment. Wall Street maintains a constructive view on Construction Partners, with the analyst consensus standing at 4 buy ratings, 2 hold ratings, and 0 sell ratings. The absence of sell recommendations combined with the post-earnings stock rally suggests the investment community is gaining confidence in the company’s ability to execute on its growth strategy.

What to Watch: Monitor execution against the substantial project backlog and organic growth sustainability as the company scales. The ability to convert pipeline into revenue while maintaining profitability margins will determine whether this quarter represents a turning point or a seasonal anomaly in Construction Partners’ earnings trajectory.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.

[ad_2]

Source link