[ad_1]

AlphaStreet Newsdesk powered by AlphaStreet Intelligence

FY26 EPS guidance – adjusted $0.70 – $0.80|Stock $2.51 (+2.0%)

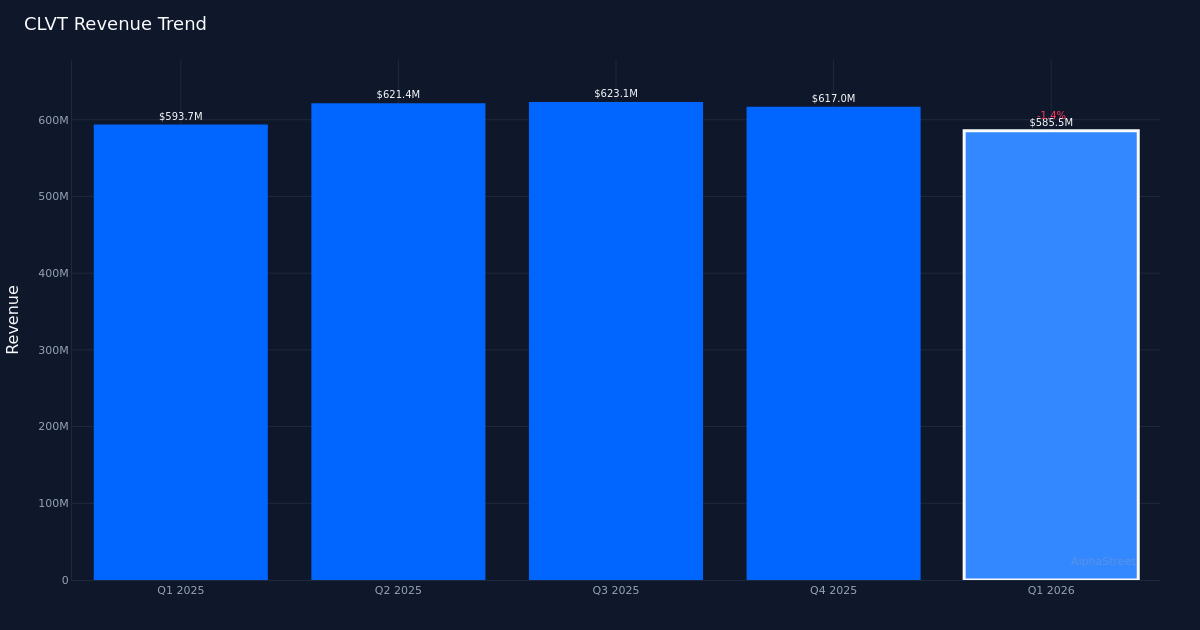

Solid beat. Clarivate Plc (NYSE: CLVT) delivered Q1 2026 adjusted diluted EPS of $0.18, surpassing Wall Street’s $0.15 estimate by 20.0%, even as the information technology services provider navigated a modest revenue headwind. The company generated $585.5M in revenue for the quarter, representing a 1.4% decrease from the $593.7M recorded in Q1 2025. Adjusted net income for the period came in at $119.3M. Shares rose 2.0% to $2.51 following the release, suggesting investors are rewarding the bottom-line outperformance despite the muted top-line growth.

Margin expansion story. The quality of this earnings beat warrants scrutiny. With revenue declining year-over-year while EPS meaningfully exceeded expectations, the outperformance appears driven primarily by operational efficiency and cost management rather than underlying demand strength. The 20.0% EPS beat against a backdrop of revenue contraction suggests margin improvement initiatives are taking hold, though institutional investors typically place greater value on revenue-driven beats that signal genuine business momentum. The company’s organic ACV growth of 1.6% for the quarter provides some reassurance that the core business retains modest growth potential, even if overall revenue hasn’t yet inflected positive.

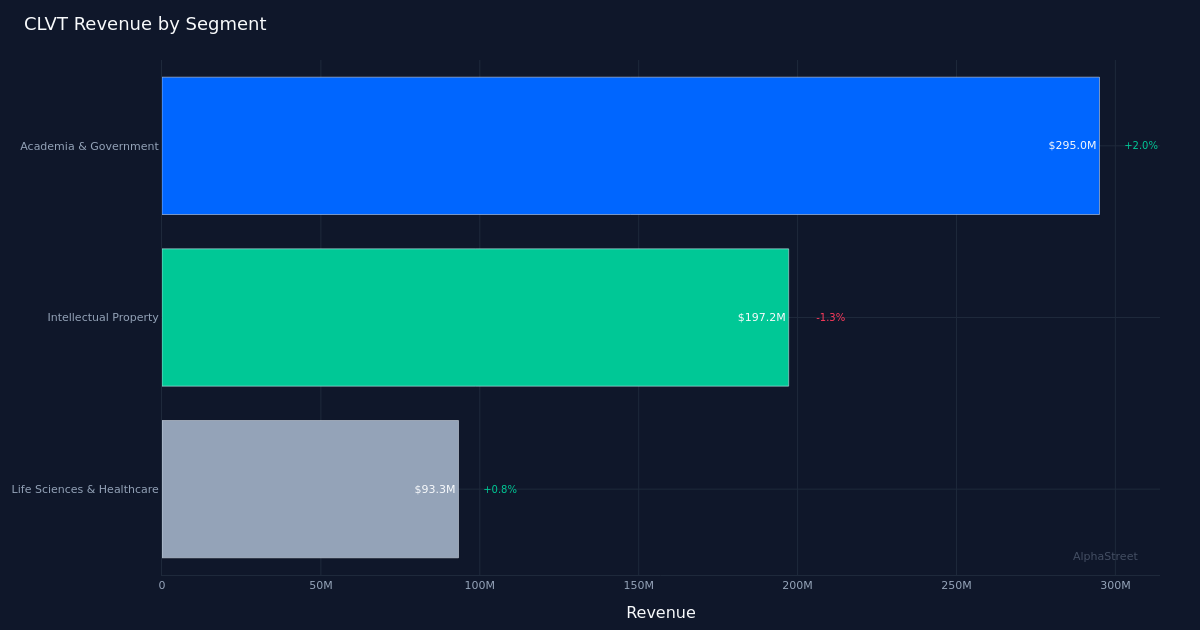

Academia segment stabilizes. Academia & Government led the business with $295.0M in revenue, up 2.0% year-over-year on an organic basis, demonstrating resilience in Clarivate’s largest vertical. This segment’s ability to post positive growth while the overall company experienced a revenue decline highlights its importance to the portfolio and suggests customer retention remains intact within the academic and public sector research communities. The segment’s performance provides a partial offset to weakness in the Intellectual Property segment.

Conservative FY outlook. Management projected FY 2026 adjusted EPS in the $0.70 to $0.80 range, with revenue expectations of $2.30B to $2.42B. The wide guidance ranges reflect continued uncertainty in the operating environment, though the midpoint of the revenue guidance implies a potential return to growth on an annual basis. The EPS guidance suggests management expects the margin expansion evident in Q1 to persist throughout the year, with profitability improvements potentially accelerating if the company can stabilize or grow its top line in coming quarters.

Street remains cautious. Wall Street consensus of 0 buy, 8 hold, and 2 sell ratings reflects persistent skepticism about Clarivate’s growth prospects and competitive positioning. The analyst community appears unconvinced that the current trajectory warrants aggressive accumulation, instead adopting a wait-and-see posture. The modest 2.0% post-earnings bounce suggests the market shares this measured view, treating the Q1 beat as incrementally positive but insufficient to fundamentally alter the investment thesis.

What to Watch: Whether Clarivate can translate margin discipline into sustainable earnings growth while reigniting revenue momentum remains the critical qestion. Q2 organic ACV trends and any acceleration in the Academia & Government segment will signal if this beat marks an inflection point or merely reflects effective cost control masking underlying demand challenges.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.

[ad_2]

Source link