[ad_1]

For Cisco Systems Inc. (NASDAQ: CSCO), 2022 was a rather challenging year when the business was hit twice by the pandemic and economic uncertainty. While reduced corporate spending due to inflationary pressures remains a concern, tech companies look set for a strong year ahead, thanks to stable demand and supply chain recovery.

Shares of the San Jose-based network marker declined ahead of next week’s earnings, after remaining on a recovery path for more than three months. But it is likely to change course after earnings and gather momentum in the coming months. CSCO offers a good dividend yield of more than 3%, which makes it an attractive investment option, especially for income investors.

Market

Over the years, the company has continued to increase its presence in overseas markets, but more than half of its profits still come from America. The accelerating digital transformation across industries bodes well for Cisco, given its strong adoption of cybersecurity and subscription-based software services.

Check out this space to read management/analyst comments on monthly reports

From Cisco’s Q1 2023 earnings conference call:

“Our portfolio is excellent and our business model is resilient, with 43% of our revenue now recurring, which is very important as we navigate the current macro environment. The hard work and dedicated commitment of our leadership team and employees over the past few years to transform our business model we look at the performance we delivered this quarter.Combined with the strength of our balance sheet and our position in the market, we have a good foundation to generate long-term results.

Q2 Report Because

Market observers, on average, estimate that Cisco has generated $ 0.85 per share in the January quarter, which is up 1% from the previous year period. The improvement represents an increase in second-quarter revenue to about $13.43 billion. That is broadly in line with the guidance issued by management in last earnings. The Q2 report is expected to be released on February 15, in the evening.

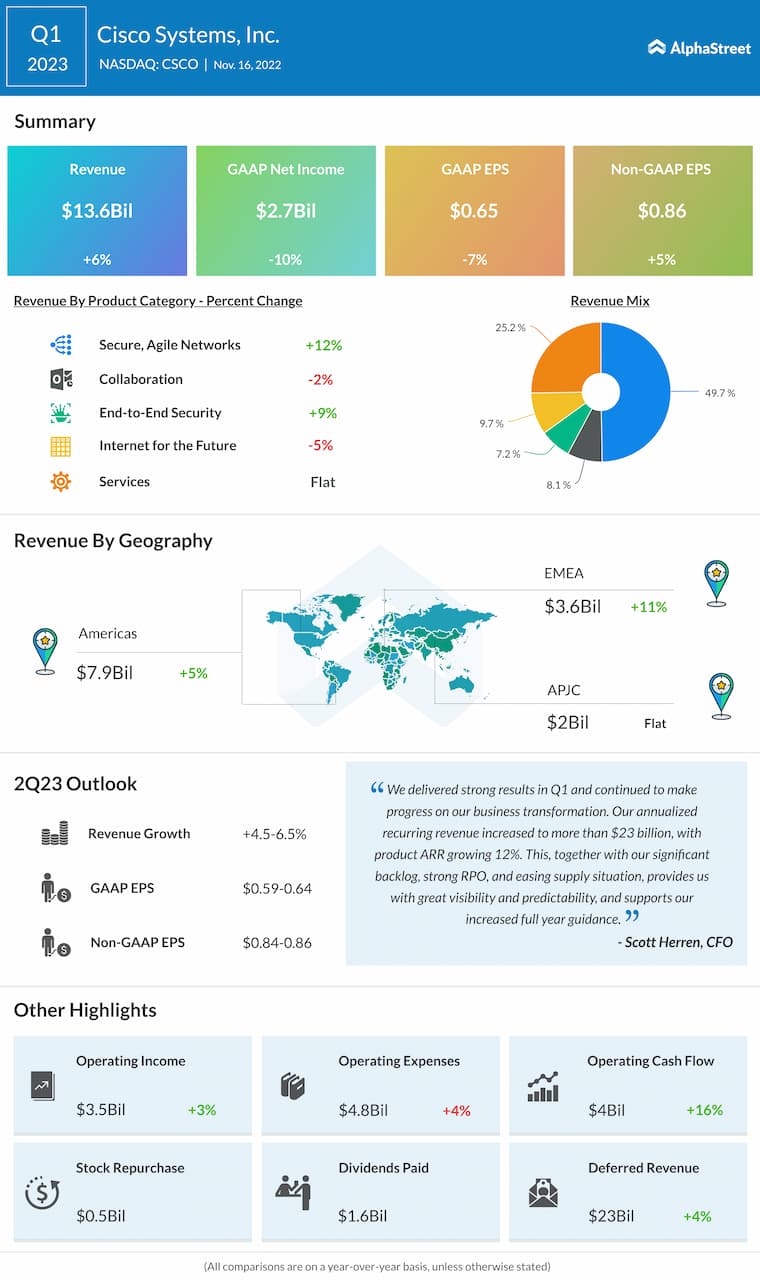

In the October quarter, the core network infrastructure business, which accounts for about 50% of total revenue, performed well. The double-digit growth marked a rebound from last quarter when the business was hit by high costs, component shortages, and supply chain issues. That, along with 9% growth in the relatively small security division, lifted total first-quarter revenue by 6% to $14 billion. Earnings rose to $0.86 per share and topped consensus forecasts, as they have done in nearly every quarter since the company began reporting results.

MSFT earnings: Microsoft’s Q2 profit falls amid weak revenue growth

CSCO opened Thursday’s session slightly below $47 and traded lower during the session. It experienced continued volatility until this year.

[ad_2]

Source link