[ad_1]

AlphaStreet Newsdesk powered by AlphaStreet Intelligence

BUDA|EPS $0.05 vs $0.03 est (+66.7%)|Rev $3.5M|Net Income $388,000

BUDA|EPS $0.05 vs $0.03 est (+66.7%)|Rev $3.5M|Net Income $388,000Stock $9.94 (+0.0%)

EPS YoY -16.7%|Rev YoY +17.7%|Net Margin 11.1%

Buda Juice delivered a solid earnings beat in Q1 2026, but the quality of that outperformance raises important questions about underlying profitability. The beverage maker posted adjusted EPS of $0.05, comfortably ahead of the $0.03 consensus estimate for a 66.7% surprise. Revenue reached $3.5M, representing growth of 17.7% year-over-year from $3.0M in Q1 2025. While the top-line acceleration merits attention, the accompanying margin compression tells a more complex story about the economics of this growth.

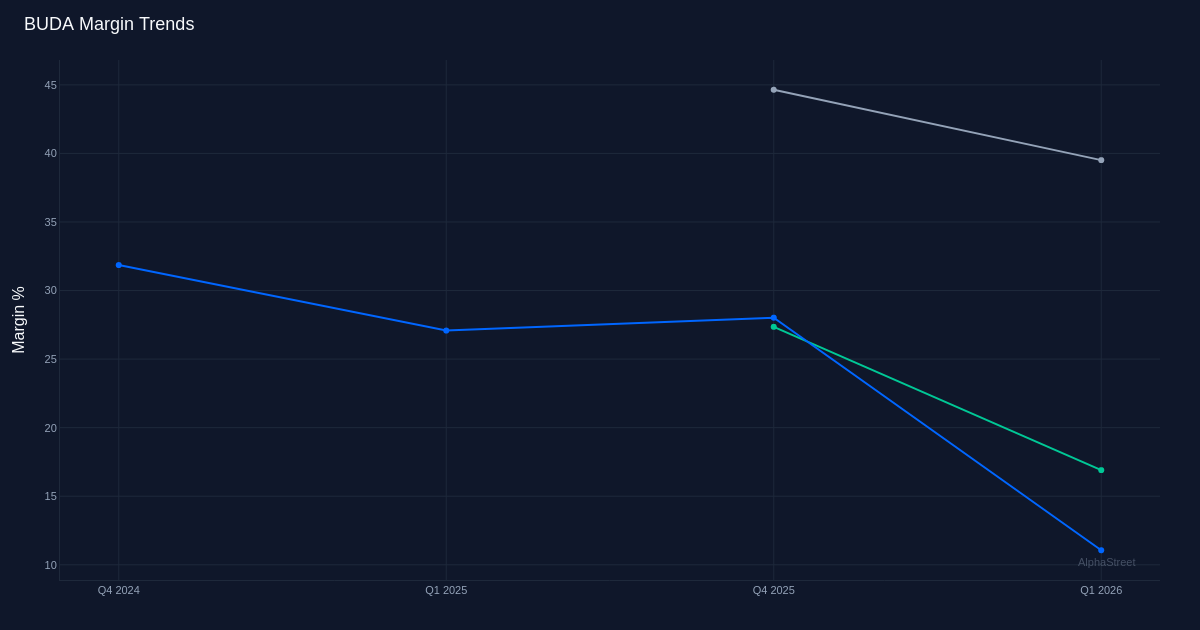

The quality of this quarter’s earnings deteriorated sharply compared to the year-ago period, with profitability metrics compressing across the board despite revenue expansion. Net margin collapsed to 11.1% from 26.9% in Q1 2025, a decline of 15.8 percentage points that transformed what should have been a strong growth story into a concerning profitability narrative. Net income fell to $388,000 from $807,000 in the prior-year quarter, meaning the company generated less absolute profit on a larger revenue base. The disconnect between revenue growth of 17.7% and the simultaneous 16.7% decline in EPS to $0.05 from $0.06 reveals that Buda Juice is sacrificing margin to chase volume. Even with gross margin holding at a respectable 39.6% and operating margin at 16.9%, the year-over-year comparison suggests either elevated input costs, aggressive promotional activity, or operational inefficiencies that management has yet to address in their commentary.

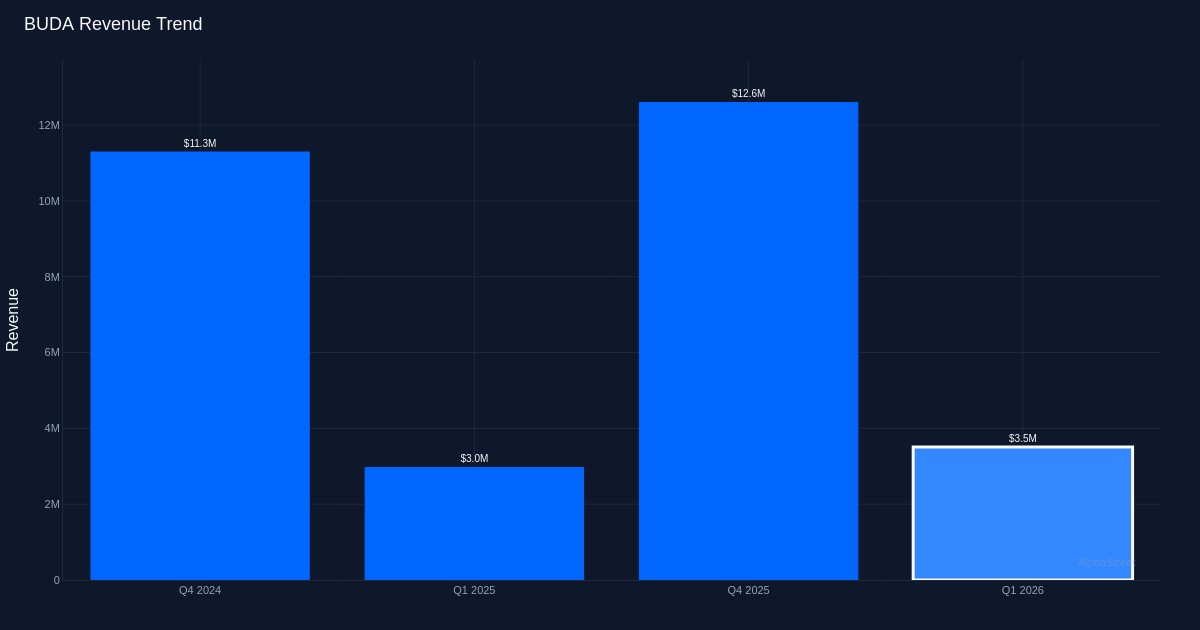

The four-quarter revenue trajectory reveals extreme volatility that complicates any assessment of sustainable growth momentum. Q1 2026 revenue of $3.5M followed Q4 2025’s $12.6M, which itself came after Q1 2025’s $3.0M and Q4 2024’s $11.3M. This pattern points to dramatic seasonal concentration in the fourth quarter, with Q4 revenue running approximately 3.6 times the Q1 run rate. The sequential decline from $12.6M to $3.5M quarter-over-quarter represents the normal seasonal pattern, but the magnitude of this swing creates significant working capital challenges and makes annualized projections treacherous. Management noted that “Revenue grew 17.7% year over year, which is about the mid teens outlook we discussed on our last earnings call,” suggesting the company is delivering on its own expectations for this seasonal trough quarter.

Cash generation provided the quarter’s most encouraging signal, with operating cash flow and free cash flow both outpacing reported earnings. Operating cash flow reached $1.3M while free cash flow hit $1.1M, representing 37.0% growth in free cash flow generation. The $1.1M in free cash flow on $388,000 in net income demonstrates that reported earnings understated the quarter’s true cash-generating ability by nearly 3x. This divergence typically indicates favorable working capital dynamics or non-cash charges depressing reported earnings, and it partially offsets concerns about margin compression. The relationship between $1.1M in free cash flow and $3.5M in revenue yields a robust cash conversion profile that suggests the business model, despite profitability challenges, generates tangible returns.

Management’s commentary focused heavily on validating their prior guidance rather than providing insight into margin dynamics. Executives emphasized that the quarter’s performance aligned with expectations, with one manager stating, “This represented a half million dollar increase in to 3.5 million from 3 million in the prior year period.” The reference to Walmart pricing—”the Walmart 12 ounce lemonade, the single serve lemonade, they price it at $1.50, actually just slightly under that”—provides a rare glimpse into the company’s retail positioning and suggests Buda Juice is competing in the value segment of the non-alcoholic beverage category. This value positioning may explain the margin pressure, as competing on price with major retailers like Walmart typically compresses margins even as it drives volume growth.

The 100% beat rate over the last quarter establishes only minimal credibility given the limited sample size. Buda Juice has now beaten estimates in 1 of 1 reported quarters, which provides no meaningful track record for assessing management’s guidance reliability or the Street’s forecasting accuracy. The significant EPS beat of 66.7% could reflect either conservative analyst estimates or genuine operational outperformance, but without additional quarters of data, investors lack the pattern recognition necessary to determine which dynamic is at play.

The muted stock reaction to a substantial earnings beat signals investor skepticism about the sustainability of current trends. Shares remained largely unchanged following the report despite the EPS surprise, suggesting the market saw through the headline beat to focus on deteriorating margins and the year-over-year decline in absolute profitability. This non-reaction typically indicates either that the beat was fully anticipated, that guidance disappointed, or that investors are focused on the quality issues evident in the margin data rather than the top-line growth story management is emphasizing.

The current quarter’s results position Buda Juice at a crossroads between growth and profitability. The company has demonstrated it can drive mid-teens revenue growth, but the 15.8 percentage point decline in net margin and the drop in absolute net income from $807,000 to $388,000 year-over-year raise fundamental questions about the economic value of that growth. With EBITDA of $700,000 and operating income of $593,000, the company maintains positive unit economics, but the trajectory is concerning. The stark seasonal pattern evident in the four-quarter trend means Q2 through Q3 will be critical in determining whether Q1’s margin compression was an anomaly or the beginning of a structural shift in the business model.

What to Watch: The key forward-looking question is whether Buda Juice can restore profitability to prior-year levels as it exits the seasonal trough. Investors should monitor net margin trajectory in Q2 2026 for signs of improvement from the 11.1% reported this quarter. The company’s ability to maintain the 37.0% free cash flow growth rate while improving reported profitability will determine whether the current valuation reflects opportunity or a value trap. Any commentary on pricing power versus promotional intensity in the retail channel will clarify whether margin pressure stems from input costs or competitive dynamics. The sustainability of the mid-teens revenue growth guidance management reiterated will also come into focus as comparisons against the high seasonal quarters of Q4 2025 approach.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.

[ad_2]

Source link