[ad_1]

AlphaStreet Newsdesk powered by AlphaStreet Intelligence

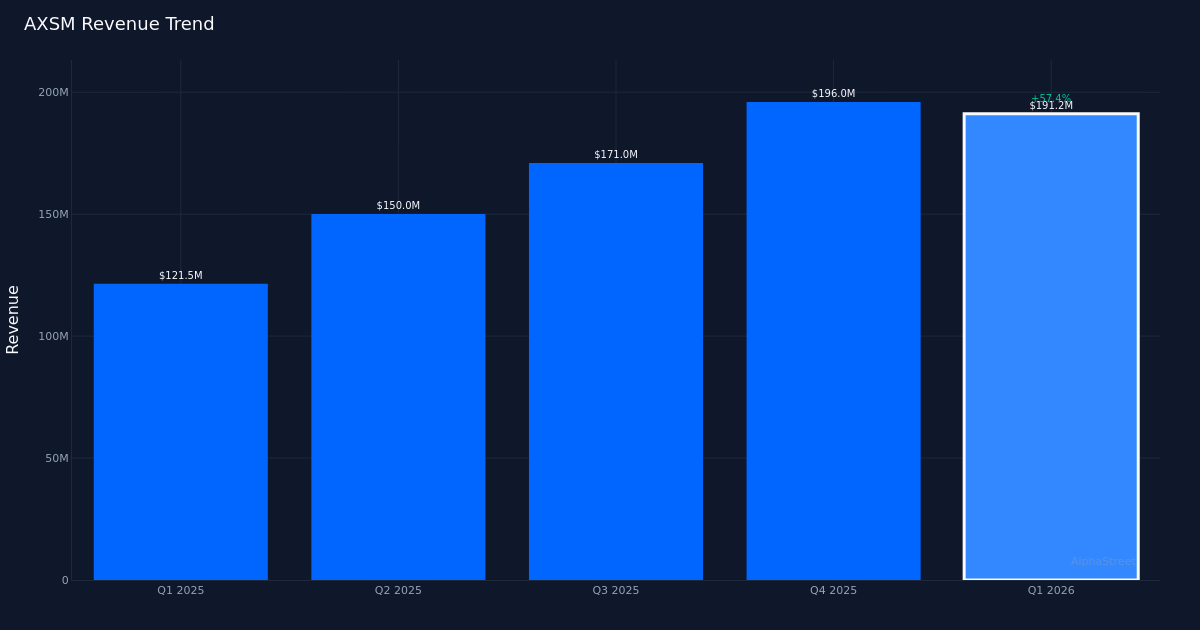

AXSM|Loss Per Share -$1.26 vs -$0.83 est (-51.8%)|Rev $191.2M vs $190.5M est (+0.3%)|Net Loss $64.5M

Mixed Quarter. Axsome Therapeutics, Inc. (NASDAQ: AXSM) delivered Q1 2026 results that highlighted the company’s commercial momentum even as profitability remains elusive. The biotechnology firm posted a diluted loss of $1.26 per share, significantly wider than the $0.83 loss analysts anticipated. Revenue of $191.2M essentially matched the $190.5M consensus, demonstrating continued top-line execution across its commercial portfolio.

Revenue Acceleration. The company’s top-line performance showed robust expansion, with total revenue climbing 57.0% from the $121.5M recorded in Q1 2025. Management emphasized the broad-based nature of this growth, stating “Total revenue for the quarter was $191.2 million, a 57% increase compared to 1Q25.” This acceleration underscores Axsome’s ability to penetrate its target markets and expand the commercial footprint of its neuropsychiatric product portfolio. The revenue match against consensus suggests the company is executing on plan despite the challenging backdrop for specialty pharmaceutical launches.

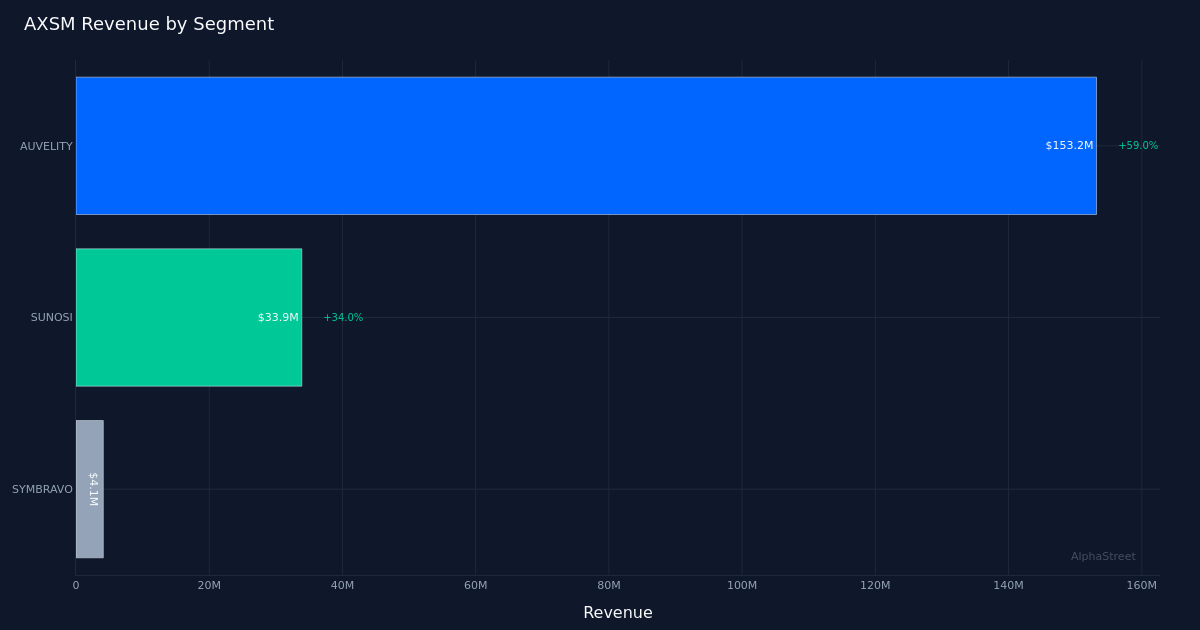

AUVELITY Dominance. The company’s flagship product AUVELITY continued to drive commercial performance, generating $153.2M in revenue during the quarter—a 59.0% year-over-year increase that outpaced the overall revenue growth rate. The depression treatment accounted for the lion’s share of Axsome’s business, with operational metrics showing 223,000 AUVELITY prescriptions written at quarter-end. This prescription volume demonstrates sustained physician adoption and patient demand, critical indicators of durability in the competitive CNS therapeutic landscape.

Profitability Pressure. The widening loss presents a more concerning picture. Axsome reported a net loss of $64.5M for the quarter, with the per-share loss of $1.26 expanding 3.3% from the $1.22 loss in Q1 2025. The deterioration in profitability despite strong revenue growth suggests that commercial expansion costs—likely including sales force expansion, marketing investments, and manufacturing scale-up—are outpacing top-line gains. The wider-than-expected loss indicates that either operating expenses exceeded internal projections or gross margins came in below plan, warranting scrutiny of the company’s path to profitability.

Commercial Execution. Despite the earnings miss, the quarter validates Axsome’s commercial strategy. The company is successfully scaling multiple products simultaneously, with management noting contributions from its broader portfolio beyond AUVELITY. For a mid-stage biotechnology company, maintaining revenue growth at these levels while building the infrastructure for a multi-product commercial platform represents meaningful progress, even as near-term profitability remains pressured.

What to Watch: The key question for investors is whether Axsome can leverage its 57% revenue growth into operating leverage. Monitor prescription trends for AUVELITY and uptake of newer products, while scrutinizing whether the company can moderate expense growth to narrow losses in subsequent quarters.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.

[ad_2]

Source link