[ad_1]

AlphaStreet Newsdesk powered by AlphaStreet Intelligence

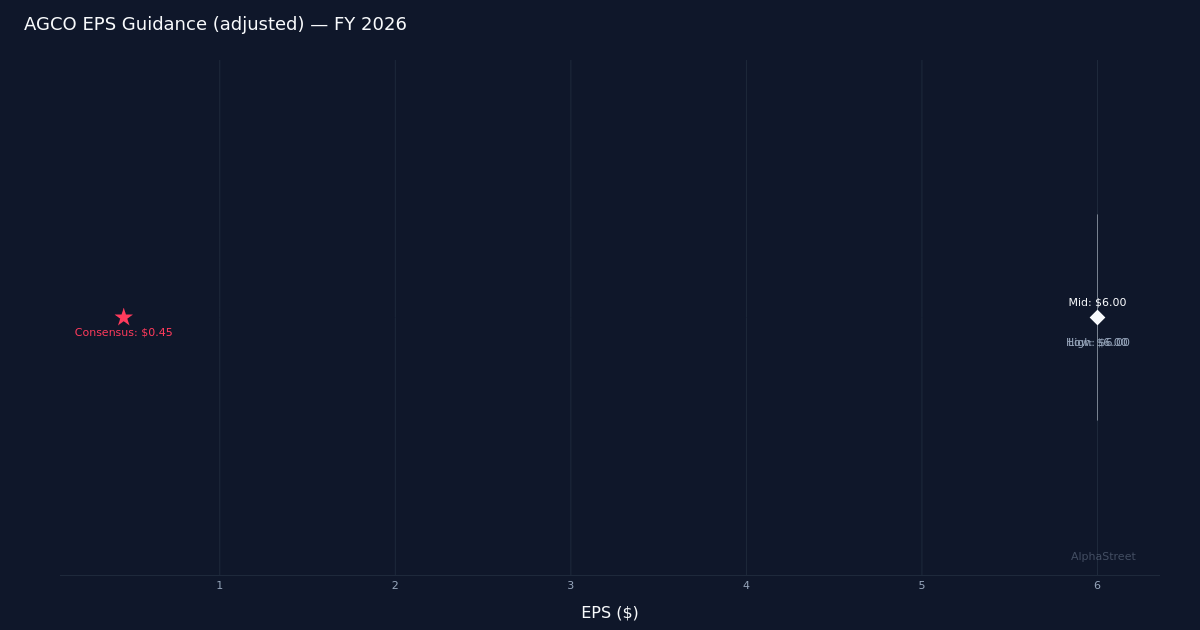

Guidance adjusted $6.00 – $6.00|Stock $121.28 (+2.3%)

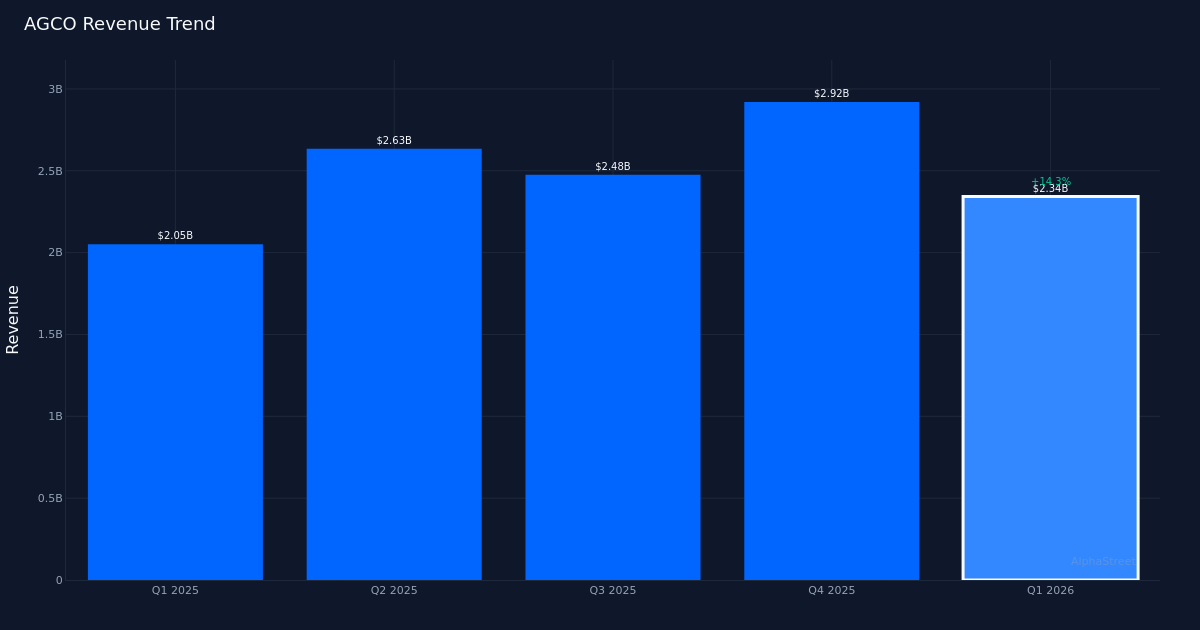

Strong Beat Signals Turnaround. Agco Corporation (NYSE:AGCO) delivered Q1 2026 adjusted earnings of $0.94 per share, crushing analysts’ $0.45 forecast by 113.6% and signaling potential momentum in the agricultural equipment cycle. The farm and heavy construction machinery manufacturer generated $2.34B in revenue for the quarter, up 14.3% from $2.05B in Q1 2025, suggesting genuine end-market recovery rather than margin engineering alone. Shares rose 2.3% to $121.28 following the release, though the modest reaction may reflect investor caution about sustainability given the cyclical nature of the agricultural equipment market.

European Strength Drives Growth. The quality of this beat deserves scrutiny, and the geographic mix provides encouraging evidence of demand-driven outperformance. Europe/Middle East led with $1.60B in revenue, up 20.3% year-over-year, representing roughly two-thirds of total company revenue and demonstrating robust market share gains in Agco’s most important region. This double-digit regional growth occurring alongside the substantial earnings beat suggests operating leverage is returning to the business as farmers navigate improved commodity price environments and refresh aging equipment fleets. The revenue expansion at this magnitude typically indicates unit volume growth rather than solely price realization, a healthier foundation for sustained profitability.

Full-Year Guidance Commands Attention. Management issued FY 2026 guidance calling for adjusted EPS of $6.00 and revenue between $10.50B and $10.70B. The midpoint of the revenue guide implies roughly $8.26B in remaining revenue across the final three quarters, requiring continued execution but appearing achievable given the Q1 momentum. The $6.00 EPS target represents a sharp acceleration from the $0.94 delivered in Q1, suggesting management anticipates typical seasonal strength in the second half as North American planting and harvesting seasons drive order activity. This guidance framework will face immediate scrutiny from the Street’s current split of 5 buy, 10 hold, and 2 sell ratings, with the hold-heavy consensus suggesting lingering skepticism about agricultural equipment demand sustainability.

Execution Trumps Skepticism. The magnitude of this earnings surprise—more than doubling Wall Street expectations—positions Agco to potentially shift sentiment among the 10 analysts maintaining hold ratings. Agricultural equipment cycles are notoriously difficult to forecast, and this quarter’s 14.3% revenue growth paired with expanding margins demonstrates management’s ability to capitalize on improving farmer economics. The path to the $6.00 full-year EPS target requires averaging $1.69 per share across the remaining three quarters, a steep climb but not unrealistic if European demand momentum persists and North American markets stabilize.

What to Watch: Q2 results will prove whether Europe’s 20.3% growth represents genuine market recovery or pulled-forward demand, while any updates to the $10.50B to $10.70B revenue range will signal management’s confidence in sustaining this unexpected momentum through agricultural equipment’s traditionally stronger back half.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.

[ad_2]

Source link