[ad_1]

AlphaStreet Newsdesk powered by AlphaStreet Intelligence

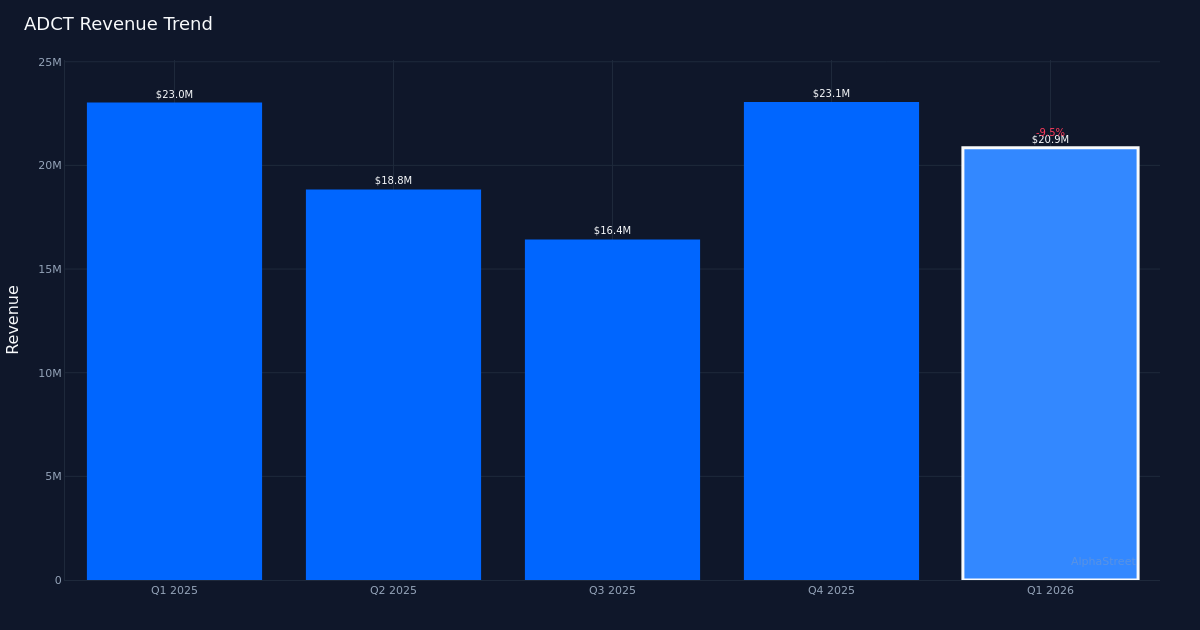

ADCT|Adj. Loss Per Share -$0.13 vs -$0.20 est (+35.0%)|Rev $20.9M vs $20.0M est (+4.3%)|Net Loss $33.0M

Narrower Loss Beats. ADC Therapeutics SA (NYSE: ADCT) reported first-quarter 2026 results that exceeded analyst expectations on both the top and bottom lines, with an adjusted loss of $0.13 per share coming in narrower than the consensus estimate of a $0.20 loss. The biotechnology company’s revenue of $20.9M topped the $20.0M analyst consensus by 4.3%, demonstrating continued commercial execution despite year-over-year headwinds. The performance reflects a mixed operational picture, with cost discipline helping to offset revenue pressure while the company advances its pipeline of antibody-drug conjugates.

Revenue Decline Continues. The top-line beat masks underlying softness in ADC Therapeutics’ commercial trajectory, with quarterly revenue declining 9.5% from $23.0M in the prior-year period. For a biotechnology company still in the early stages of commercializing its lead products, this year-over-year contraction raises questions about market penetration and competitive dynamics in the company’s targeted oncology indications. The ability to edge past Street estimates provides modest reassurance that management is maintaining realistic guidance, but the declining revenue trend will need to stabilize for the growth narrative to regain momentum among institutional investors.

Cost Management Drives Beat. The company posted an adjusted net loss of $19.7M for the quarter. The magnitude of the earnings beat appears primarily driven by expense management rather than revenue outperformance, given the modest top-line beat of just 4.3%. While cost discipline is a necessary component of extending the cash runway for pre-profitable biotechnology firms, investors typically assign greater value to revenue-driven beats that signal strengthening commercial traction. The narrower loss compared to analyst models suggests ADC Therapeutics is successfully controlling burn rate as it works to expand market adoption of its therapies.

Pipeline Progress Critical. With commercial revenue under pressure, ADC Therapeutics’ path to sustained growth will depend heavily on pipeline advancement and potential label expansions for existing products. The biotechnology sector demands continuous clinical progress to support valuation multiples, particularly when established products face growth challenges. The company’s antibody-drug conjugate platform represents significant therapeutic potential in oncology, but translating that scientific promise into commercial success requires both regulatory wins and market acceptance across multiple indications.

What to Watch: Investors should monitor whether ADC Therapeutics can reverse the year-over-year revenue decline in coming quarters while maintaining the expense discipline that drove the first-quarter beat. The company’s ability to stabilize and ultimately grow its commercial base will determine whether the current valuation reflects a turnaround opportunity or continued headwinds in a competitive oncology landscape.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.

[ad_2]

Source link