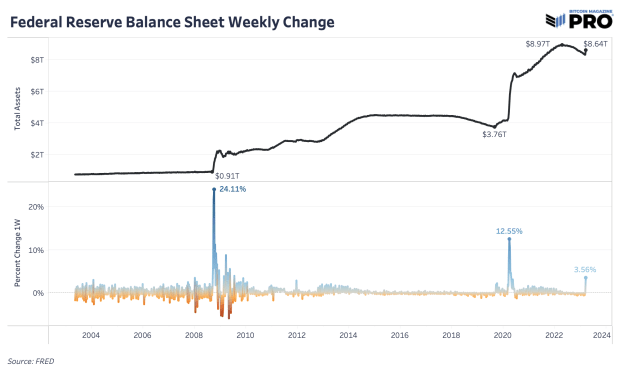

The Federal Reserve’s balance sheet increased by $300 billion in a week, sparking debate over whether the move qualifies as quantitative easing.

The following article is an excerpt from the latest issue of Bitcoin Magazine PRO, Bitcoin Magazine’s premium market newsletter. To be the first to receive this insight and other on-chain bitcoin market analysis straight to your inbox, subscribe now.

The Lender Of Last Resort

Just days after the collapse of Silicon Valley Bank and the establishment of the Bank Term Funding Program (BTFP), there was a significant increase in the Federal Reserve’s balance sheet after a year of decline through quantitative tightening (QT). The PTSD of extensive quantitative easing (QE) caused many to sound the alarm, but the changes in the Fed’s balance sheet were more than the new regime’s change in monetary policy. In absolute terms, this is the biggest increase in the balance sheet that we have seen since March 2020 and in relative terms, it is the outlier that is catching everyone’s attention.

What’s important is that this is very different from the QE asset purchases and easy money stimulus at near-zero interest rates that we’ve been experiencing for the past decade. This is about preferred banks that need liquidity when there are economic conditions and these banks obtain short-term loans with the aim of covering deposits and repaying loans quickly. It does not directly buy securities to continue the balance sheet of the Fed, but the balance sheet assets that should be short-lived while continuing the QT policy.

However, this is an expansion of the balance sheet and an increase in liquidity in the short term – perhaps only a “temporary” measure (still to be determined). At the very least, this injection of liquidity helps institutions avoid being forced sellers of securities. Whether that is QE, pseudo QE, or no QE is beside the point. The system is showing its fragility again and governments must act to avoid facing systemic risks. In the short term, assets that thrive on increased liquidity, like bitcoin and the Nasdaq, which have been tearing higher at the same time.

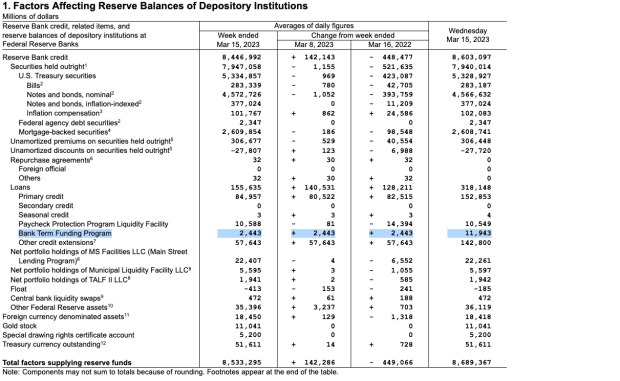

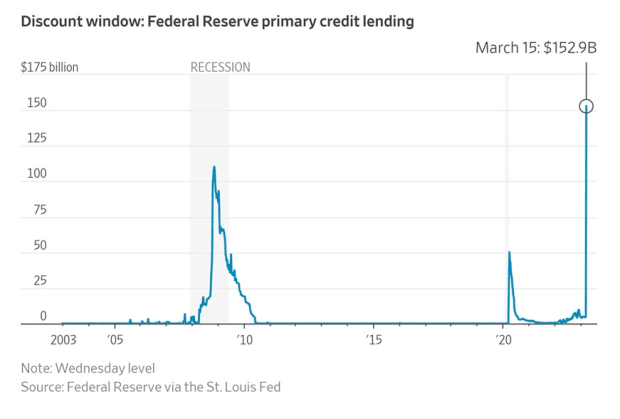

A certain increase in the Fed’s balance sheet is due to an increase in short-term loans through the Fed’s discount window, loans to FDIC bridge banks for Silicon Valley Bank and Signature Bank and the Bank Term Funding Program. Discount window loans of $152.8 billion, FDIC bridge bank loans of $142.8 billion and BTFP loans of $11.9 billion for a total of more than $300 billion.

A more alarming increase is in discount window lending because it is the last resort, a high-cost liquidity option for banks to cover deposits. This is the largest discount window loan on record. The banks that use the window remain anonymous because of the legal stigma of finding out who needs short-term liquidity.

It brought back fresh memories of the 2019 emergency liquidity injection and intervention by the Fed into the repo market to stabilize cash demand and short-term lending activity. The repo market is the main overnight financing method between banks and other institutions.

Download your FREE “Banking Crisis Survival Guide” Today!

Get a copy of the full report here.

The upcoming FOMC meeting

Markets still expect a 25 bps rate hike at next week’s FOMC meeting. All in all, the market turmoil has so far not proven to be “damaging enough”, which would require an emergency pivot from the central banker.

On track to bring inflation back to the 2% target, the month-on-month core CPI still rose in February while initial jobless claims and unemployment were not high. Wage growth, especially in the service sector, still remained fairly strong at a 3-month annual rate of 6% last month. Even if it’s down a bit, more unemployment is where we need to see more weakness in the labor market to allow for lower wage growth.

We may be a long way from the end of this year’s chaos and volatility, as each month brings a new level of uncertainty to the markets. This is the first sign of a system that needs Federal Reserve intervention and quick action. It certainly won’t be the last in 2023.

That sums up the quote from the new edition of Bitcoin Magazine PRO. Subscribe now to receive PRO articles directly in your inbox.

Relevant past articles:

- Banking Crisis Survival Guide

- PRO Market Key of the Week: Market Says Tightening Is Over

- Biggest Bank Failure Since 2008 Sparks Market-Wide Fears

- Banking Trouble Brewing In Crypto-Land

- A Tale of Tail Risks: The Fiat Prisoner’s Dilemma

- Bank Of Japan Blinks And Markets Tremble

- Bubble Everything: Markets at the Crossroads

- Silvergate Bank Faces Savings As Share Price Falls

- Counterparty Risk Happens Fast

- No Average Recession: Popping the Biggest Financial Bubble in History