[ad_1]

AlphaStreet Newsdesk powered by AlphaStreet Intelligence

Stock $2.75 (-9.2%)

EPS YoY +0.0%|Rev YoY -4.7%|Net Margin -352.4%

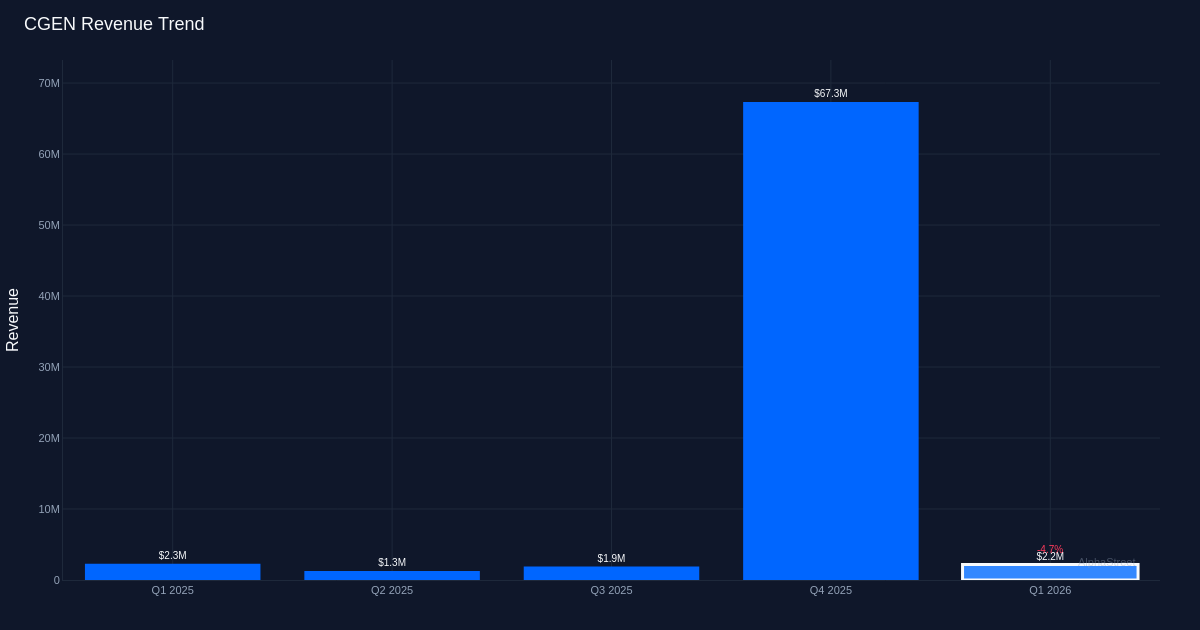

Compugen Ltd. (CGEN) missed Q1 2026 earnings expectations, reporting a loss of $0.08 per share against the consensus estimate of a $0.07 loss, marking a 14.3% miss that sent shares down 9.2%. The biotechnology company’s revenue of $2.2 million declined 4.7% year-over-year, continuing a pattern of anemic top-line performance that has plagued the clinical-stage company throughout 2025. The miss extends Compugen’s recent track record of failing to meet Wall Street’s benchmarks, with zero beats in its last quarter reported.

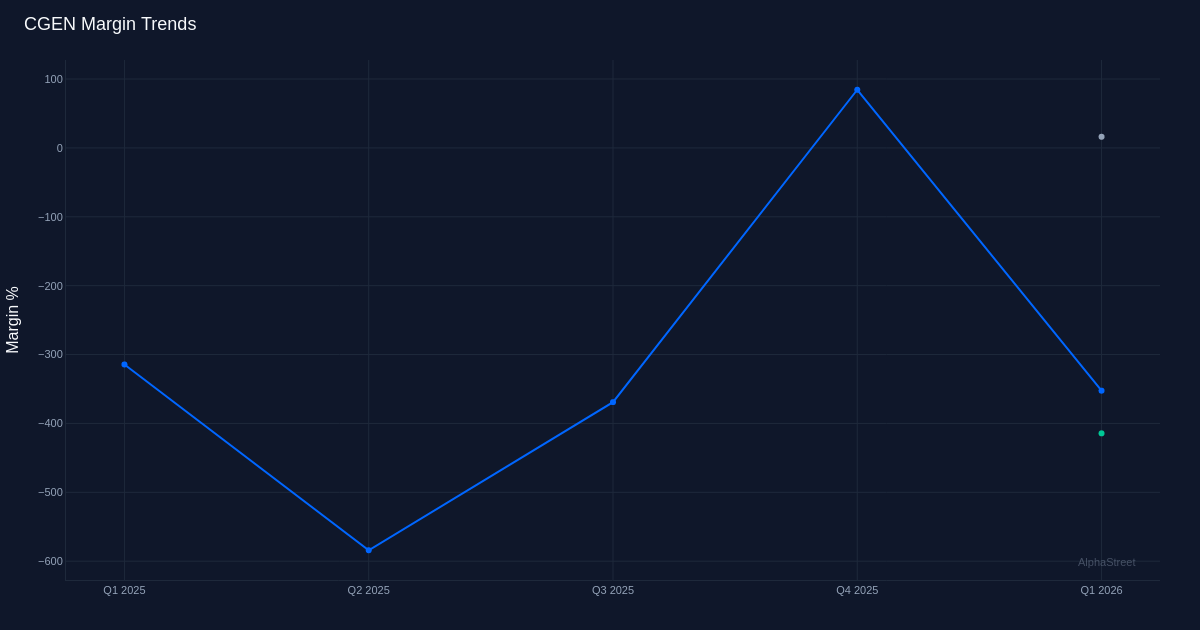

The earnings quality picture reveals a deteriorating cost structure overwhelming minimal revenue generation. Net margin compressed dramatically to negative 350.0% compared to negative 313.0% in the year-ago quarter, representing a 37 percentage point deterioration. Operating margin deteriorated even more severely to negative 409.9%, suggesting the company’s research and development spending is accelerating while revenue remains flat. Management acknowledged this dynamic, noting that “R and D expenses for the first quarter of 2026 were approximately $6.9 million compared to approximately $5.8 billion in the first quarter of 2025.” The net loss widened to $7.7 million from $7.2 million year-over-year, while gross margin of 16.0% on gross profit of just $352,000 indicates the company generates minimal contribution from its collaboration and licensing revenue to offset its substantial operating expenses.

The loss per share remaining flat at $0.08 year-over-year masks underlying deterioration in the business model. While the headline EPS figure suggests stability, the widening net loss from $7.2 million to $7.7 million indicates the company required additional share dilution or a larger share base to maintain the same per-share loss figure. This dynamic is particularly concerning for a clinical-stage biotechnology company that requires continuous capital infusion to fund trials. The operating loss expanded alongside rising R&D spending, suggesting Compugen is in an investment phase for its pipeline without corresponding revenue growth to partially offset these expenses.

Cost management showed modest discipline in general and administrative functions. Management noted that “our GNA expenses for the first quarter of 2026 were approximately $2.3 million compared to approximately $2.4 million for the comparable period in 2025,” representing a slight reduction. However, this $100,000 savings pales against the rising R&D expenditures and provides insufficient offset to prevent margin compression. For a company at Compugen’s stage with minimal revenue, the burden of proof lies in demonstrating clinical progress that justifies the cash burn rate rather than incremental G&A efficiency.

Clinical trial progress remains the central value driver, with management maintaining timeline guidance despite declining to update enrollment metrics. When pressed on trial enrollment, management stated “we’re not commenting at this point in time, but I will say to you that we are on track for our interim analysis as planned in the first quarter of 2027.” This non-disclosure on enrollment specifics while reaffirming the Q1 2027 interim analysis timeline suggests either confidence in meeting milestones or strategic ambiguity to manage investor expectations. The interim analysis represents the critical near-term catalyst that will determine whether Compugen’s current cash burn rate translates into value creation or further dilution.

The 9.2% stock decline to $2.75 reflects investor frustration with the earnings miss and absence of tangible progress markers. For a clinical-stage biotechnology company trading at this price level, the market is signaling skepticism about either the probability of clinical success or the company’s ability to reach data readouts without significant additional dilution. The Q4 2025 revenue spike that generated a profit of $0.60 per share and $56.8 million in net income now appears to be a non-recurring event, resetting investor expectations back to a loss-making profile until meaningful clinical catalysts materialize.

What to Watch: The Q1 2027 interim analysis timeline represents the make-or-break catalyst for Compugen’s investment thesis. Investors should monitor any updates on clinical trial enrollment progress, cash runway sufficiency to reach the interim readout without additional dilution, and whether the company secures additional collaboration revenue to extend its financial flexibility. Any disclosure on the nature of the Q4 2025 revenue spike and whether similar milestone payments are achievable would provide crucial context for modeling sustainable revenue potential. The relationship between R&D spending trajectory and clinical trial advancement will determine whether the current burn rate translates into value creation or simply accelerates the timeline to the next capital raise.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.

[ad_2]

Source link