[ad_1]

AlphaStreet Newsdesk powered by AlphaStreet Intelligence

IDCC|EPS $2.57 vs $1.74 est (+47.7%)|Rev $205.4M|Net Income $75.3M

IDCC|EPS $2.57 vs $1.74 est (+47.7%)|Rev $205.4M|Net Income $75.3MFY26 EPS Guidance – GAAP $5.77 – $8.51|Stock $305.15 (-13.5%)

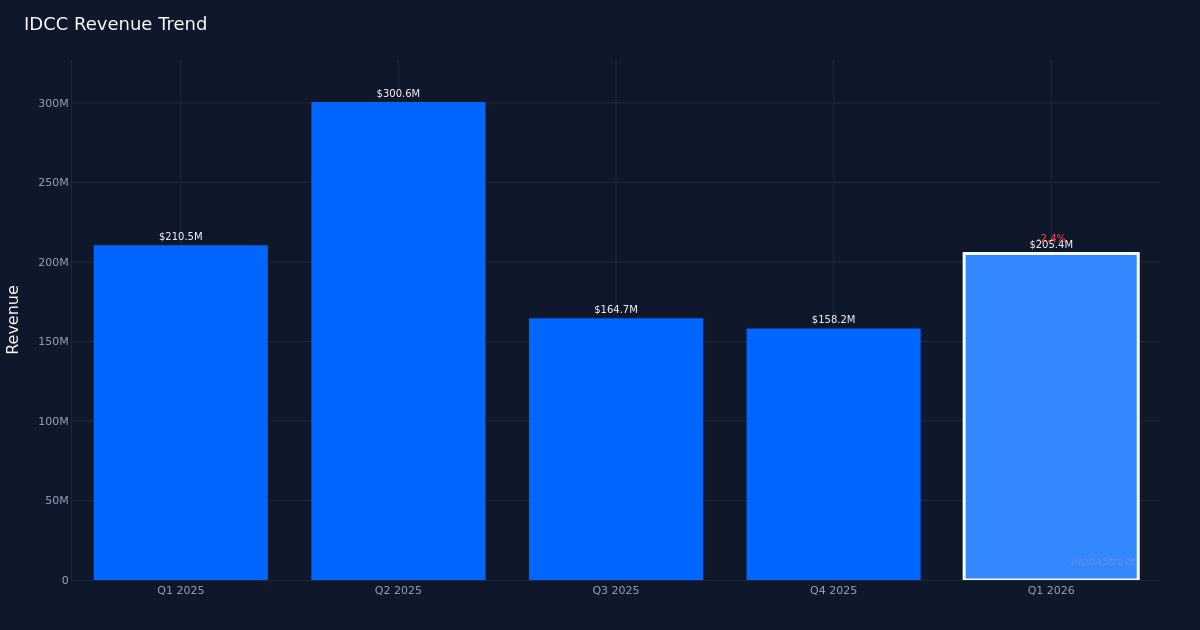

Earnings Beat Shines. InterDigital, Inc. (IDCC) delivered Q1 2026 non-GAAP earnings of $2.57 per share, surpassing analysts’ $1.74 forecast and representing a beat by 47.7%. Revenue totaled $205.4M for the quarter, with bottom-line profit coming in at $75.3M. The impressive earnings outperformance demonstrates the company’s ability to extract profitability even amid modest revenue headwinds, though the top-line performance reveals underlying challenges in the company’s core licensing business.

Revenue Softness Persists. The $205.4M quarterly revenue represents a 2.4% decrease from the $210.5M recorded in Q1 2025, signaling continued pressure on the company’s licensing agreements. While the earnings beat is notable, the revenue decline tempers enthusiasm, as true operational excellence manifests through top-line expansion rather than margin management alone. Annualized recurring revenue (ARR) was $567 for the quarter, providing a forward-looking indicator of contract stability as the company navigates patent licensing cycles.

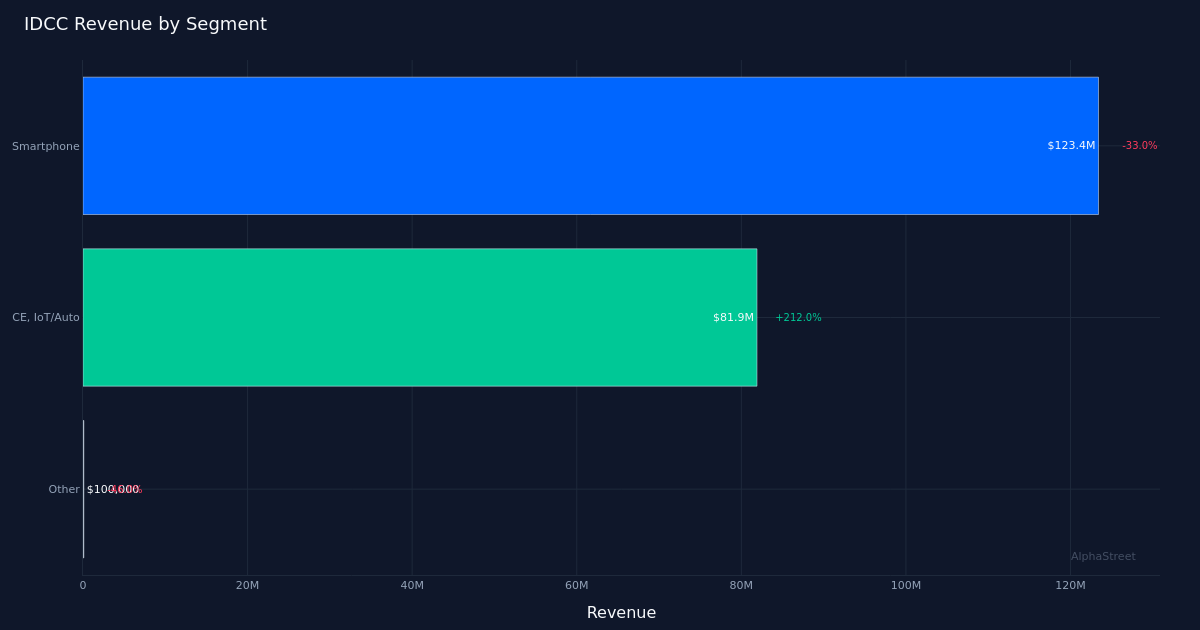

Smartphone Segment Struggles. The Smartphone segment, which led with $123.4M in revenue, experienced a sharp 33.0% year-over-year decline, representing the most significant headwind to consolidated performance. The company recorded $492 million of smartphone ARR at quarter-end, a metric that will be critical to monitor as smartphone manufacturers increasingly challenge patent licensing terms and seek more favorable royalty arrangements. This segment’s weakness explains much of the revenue shortfall and raises questions about the sustainability of the company’s traditional licensing model in its largest market.

Full-Year Guidance Provided. Management guided FY 2026 EPS (GAAP) to $5.77 to $8.51, a notably wide range that reflects uncertainty around licensing agreement timing and potential settlement outcomes. Revenue guidance for FY 2026 was set at $675.0M to $775.0M, offering a $100M spread that underscores the lumpy nature of patent licensing revenue recognition. The midpoint of the revenue guidance suggests management anticipates sequential improvement from Q1’s run rate, though investors will scrutinize whether new agreements materialize to support the upper end of the range.

Market Reacts Negatively. Despite the substantial earnings beat, shares traded at $305.15, down 13.5%, indicating investors focused on the revenue decline and smartphone segment weakness rather than bottom-line outperformance. The market’s harsh response suggests concerns about the durability of earnings if revenue continues to contract, particularly given the concentration risk in smartphone licensing. Wall Street consensus stands at 5 buy, 1 hold, 0 sell, though this harsh post-earnings selloff may prompt analyst revisions.

What to Watch: The trajectory of Smartphone ARR renewals and whether management can secure new licensing agreements to offset the 33.0% segment decline will determine if the wide FY 2026 guidance range resolves toward the upper or lower bound, making Q2 commentary on pipeline conversion critical for restoring investor confidence.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.

[ad_2]

Source link