[ad_1]

Aviva (LSE:AV.) shares have delivered a strong long-term return. Once seen as a dull income stock, the share price has risen 56% over five years, turning a £7,500 investment into £11,700.

But thatâs only part of the story. Over the same period, investors would also have received £3,025 in dividends, lifting the total return to almost double the original investment. Not bad for a âboringâ stock. The issue now is whether the insurer can keep compounding from here.

Growing dividend

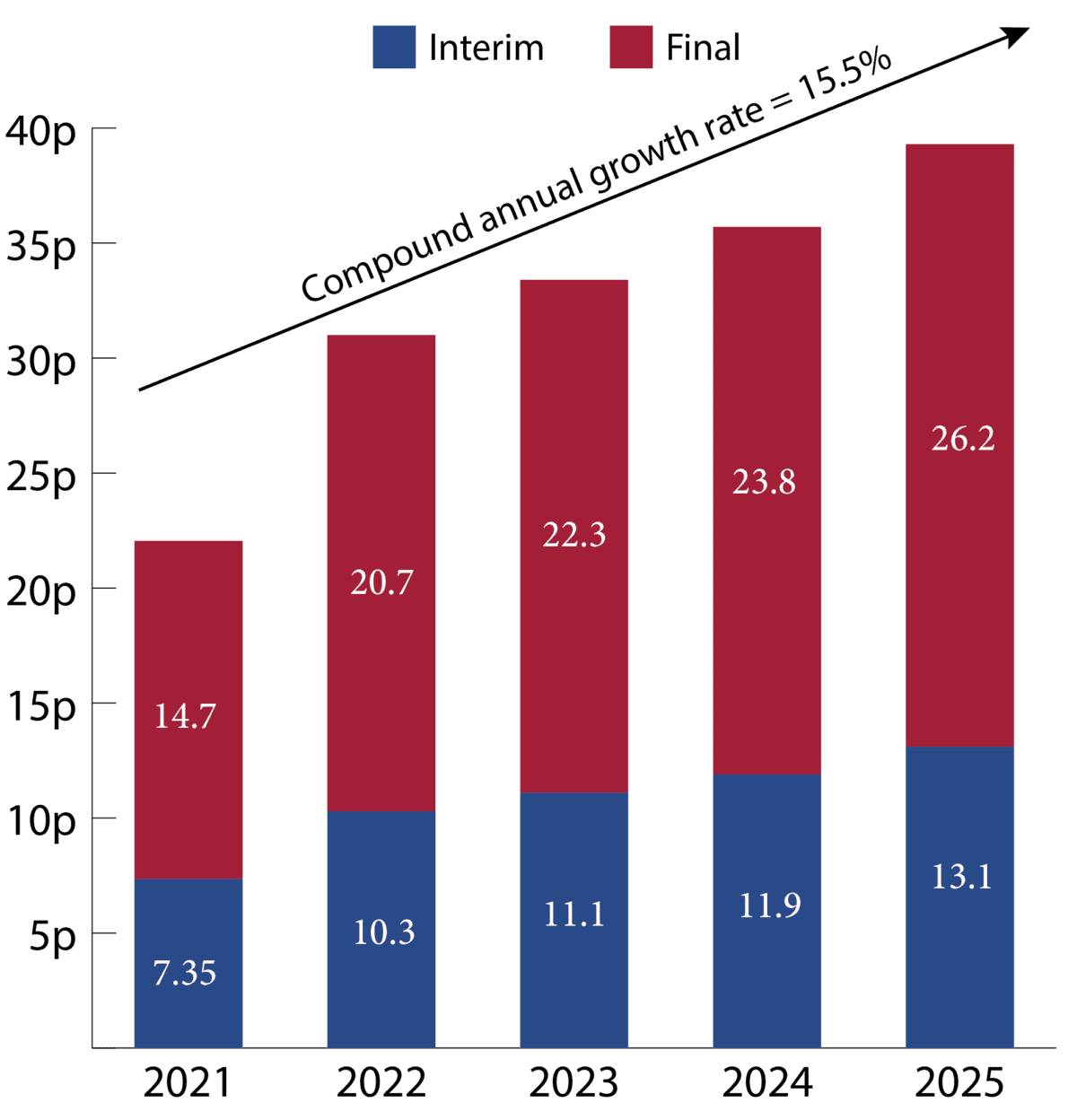

As the following chart shows, the company has delivered strong dividend compounding in recent years, with dividends per share growing at a compound annual rate of 15.5%.

Chart generated by author

This has not come from luck or one-off gains. It reflects a deeper shift taking place within the business as it moves towards a more capital-light model.

That shift matters because it changes the quality of the earnings base supporting the dividend. Rather than relying purely on traditional, capital-heavy insurance returns, a growing share of profits now comes from wealth, pensions and fee-based businesses.

These areas generate more predictable cash flows and require less balance sheet strain, which in turn supports higher and more sustainable capital returns over time.

In simple terms, the company isnât just paying a dividend â itâs steadily building the capacity to grow it.

Diversified business model

What stands out in Avivaâs latest update is how broad-based the progress has become. Management has already delivered its 2026 targets a full year early and has upgraded its medium-term ambitions. That matters because it signals execution is running ahead of expectations.

Crucially, all parts of the business are now firing on all cylinders. General insurance continues to benefit from scale advantages and disciplined underwriting. Wealth is growing strongly, supported by rising inflows and assets. Retirement and protection also continue to deliver steady, recurring earnings.

In other words, this is no longer a single-driver insurance story.

The key takeaway is that performance is now coming from across the group at the same time, rather than relying on one core engine. That creates a more resilient and self-reinforcing earnings base.

The result is a business that’s not just growing, but compounding faster than the market currently expects.

What could go wrong?

The main risk for Aviva is no longer whether the business is improving (it clearly is) but whether too much of that improvement is already reflected in expectations.

The group has already delivered its 2026 targets ahead of schedule, which raises the bar for future performance. At this stage, even a small slowdown in earnings momentum or capital generation could lead to volatility in sentiment.

There are also more traditional risks. Insurance profitability can be impacted by higher claims inflation, particularly in motor and health. Investment returns also remain sensitive to movements in bond yields and wider financial markets.

Bottom line

Aviva has already delivered a significant transformation in recent years, and the financial results increasingly reflect that shift.

The key question for investors is whether the companyâs improvement is already reflected in the share price. With earnings momentum, capital strength and diversified cash generation all moving in the right direction, itâs certainly a business investors may want to take a closer look at. But itâs not the only opportunity on my radar right now.

The post £7,500 invested in Aviva shares 5 years ago is now worth⦠appeared first on The Motley Fool UK.

Should you invest £1,000 in Aviva plc right now?

When investing expert Mark Rogers has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for nearly a decade has provided thousands of paying members with top stock recommendations from the UK and US markets.

And right now, Mark thinks there are 6 standout stocks that investors should consider buying. Want to see if Aviva plc made the list?

.custom-cta-button p

margin-bottom: 0 !important;

color:#cc0000;

div.entry-footer div.textwidget div.braze-content-card div.wp-block-custom-block-collection-presentational-card

padding: 0 !important;

margin: 0 !important;

More reading

- 5 years ago, £5,000 bought 1,231 Aviva shares. But how many would it buy now?

- How much do you need to invest each month into FTSE 100 shares to aim for a million?

- £5,000 invested in Legal & General shares 5 years ago is now worthâ¦

- £5,000 invested in Aviva shares a month ago is now worthâ¦

- Is a £100,000 SIPP big enough to retire on?

Andrew Mackie has positions in Aviva Plc. The Motley Fool UK has no position in any of the shares mentioned. Views expressed on the companies mentioned in this article are those of the writer and therefore may differ from the official recommendations we make in our subscription services such as Share Advisor, Hidden Winners and Pro. Here at The Motley Fool we believe that considering a diverse range of insights makes us better investors.

[ad_2]

Source link