[ad_1]

Tesco (LSE:TSCO) shares rose by just 1% on Wednesday 8 April. Meanwhile, Marks & Spencer was up nearly 7%.

So, what’s happening? Let’s explore.

It was never beaten up

When the conflict started in the Gulf, markets fell. But it wasn’t equal. In fact, some stocks gained, such as oil and shipping.

Tesco wasn’t a gainer, but investors were slower to sell their shares in the FTSE 100 grocer. And that’s all due to risk.

Tesco sells groceries. People bought them before the war, during it, and they’ll keep buying them now. That predictability makes it what fund managers call a defensive stock â one with low sensitivity to the economic cycle. When the world turns uncertain, money tends to flow towards stocks like Tesco rather than away from them. It’s not exciting, but it’s reliable.

That dynamic protected Tesco on the way down. The same dynamic is working against it today. The ceasefire is a risk-on event â investors are pouring back into the stocks that sold off hardest: banks, airlines, housebuilders. Tesco didn’t sell off hard, so it doesn’t snap back hard. You can’t recover ground you never lost.

In practice there is some additional nuance here. Tesco has greater cost-efficiencies than its peers and in the event of sustained cost inflation, customers may trade down from Marks & Spencer to peers like Tesco.

However, higher oil and energy prices undoubtedly hurt the supermarket giant. It has a logistics fleet, deliveries, and fridges to run.

Trading very close to fair value

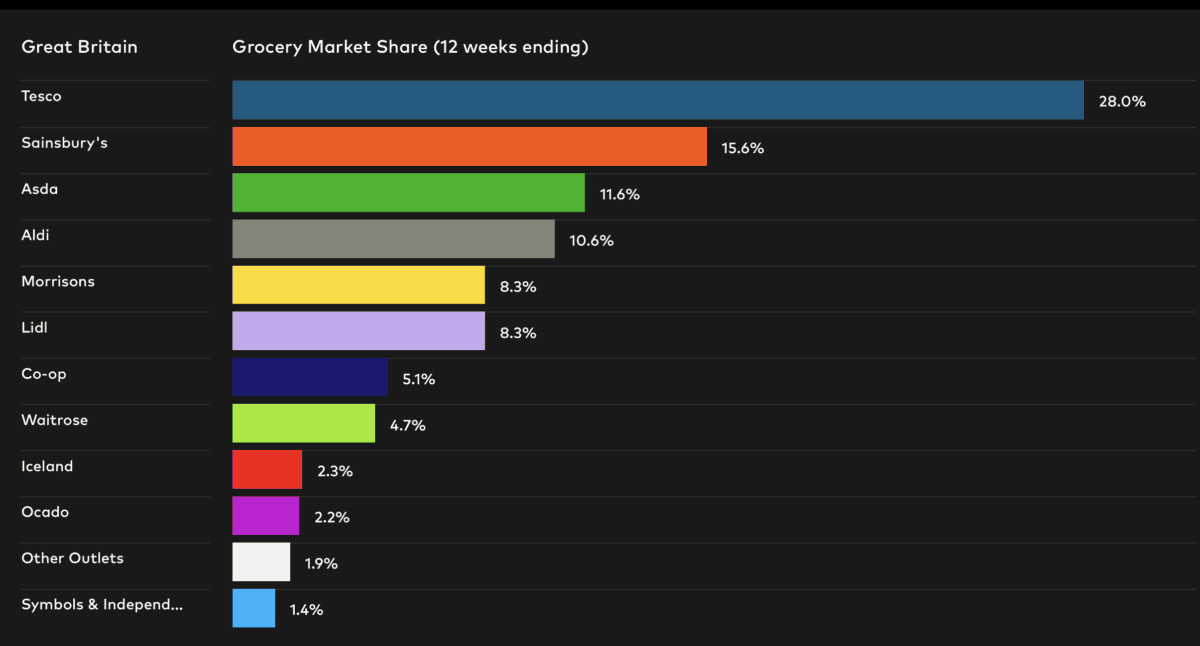

Tesco is a British champion. It’s an operational masterpiece and the brand strength is pretty much unmatched. It has also proven its ability to fight off competition from peers like Lidl and Aldi. Because of this, it deserves to trade at something of a premium to its peers.

It’s also a phenomenally consistent performer. Revenue has grown in every year since the pandemic and it’s forecasted to do the same in 2026 and 2027.

However, the difficulty is knowing how big that premium should be. Tesco is currently trading around 15.3 times forward earnings, offers a 3.3% dividend yield — covered 1.99 times by earnings — and has £10.3bn in net debt — that’s around 11 times net income.

At the other end of the scale, there’s Marks & Spencer. It trades a 10.3 times forward earnings, offers a 1.96% dividend yield — covered 5.04 times by earnings — and carries a net debt position of £2.5bn — that’s around 6 times net income.

My take

Tesco is an incredible company. However, I’m starting to think that the premium is a little stretched. Institutional analysts agree with the stock trading just 1% above the current price. It might still be worth considering, but I think there’s definitely better value to be found elsewhere.

The post Up just 1%: what’s going on with Tesco shares now? appeared first on The Motley Fool UK.

Should you invest £1,000 in Tesco PLC right now?

When investing expert Mark Rogers has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for nearly a decade has provided thousands of paying members with top stock recommendations from the UK and US markets.

And right now, Mark thinks there are 6 standout stocks that investors should consider buying. Want to see if Tesco PLC made the list?

.custom-cta-button p

margin-bottom: 0 !important;

color:#cc0000;

div.entry-footer div.textwidget div.braze-content-card div.wp-block-custom-block-collection-presentational-card

padding: 0 !important;

margin: 0 !important;

More reading

- Under £5 now! Hereâs why I think Tescoâs share price should be trading closer to £7

- £10,000 invested in red-hot Tesco shares just 1 week ago is now worthâ¦

- How much would someone need in a Stocks and Shares ISA to target an annual income of £20,855?

- New to investing? Here’s how to use the stock market to try and generate a second income

- £5,000 invested in a Stocks and Shares ISA during Covid is now worth…

James Fox has positions in Marks And Spencer Group Plc. The Motley Fool UK has recommended Marks And Spencer Group Plc and Tesco Plc. Views expressed on the companies mentioned in this article are those of the writer and therefore may differ from the official recommendations we make in our subscription services such as Share Advisor, Hidden Winners and Pro. Here at The Motley Fool we believe that considering a diverse range of insights makes us better investors.

[ad_2]

Source link