Below is an excerpt from the latest issue of Bitcoin Magazine PRO, Bitcoin Magazine premium market newsletter. To be the first to receive this insight and other on-chain bitcoin market analysis straight to your inbox, subscribe now.

As we enter 2023, we want to highlight the latest bitcoin volume and volatility situation after the recent capitulation wave. The last time we touched on these dynamics was in “The Bitcoin Ghost Town” in October, where we highlighted that very low volumes and periods of low volatility in the price of bitcoin, GBTC and the options market were signs of the next leg. It was played in early November.

Fast forward and the trend of declining volume and low volatility is back. Although this could be an indication of another lower leg coming to the market, it is more likely to indicate a complacent and collapsing market that few participants want to touch.

Even during the November 2021 capitulation period, there is a period of low volatility. Sometimes the most painful part of the market is when you have to wait for a clear trend change. Bitcoin prices are experiencing pain because we haven’t seen the kind of bursts in market volatility that have defined market pivots and major directional movements in the past.

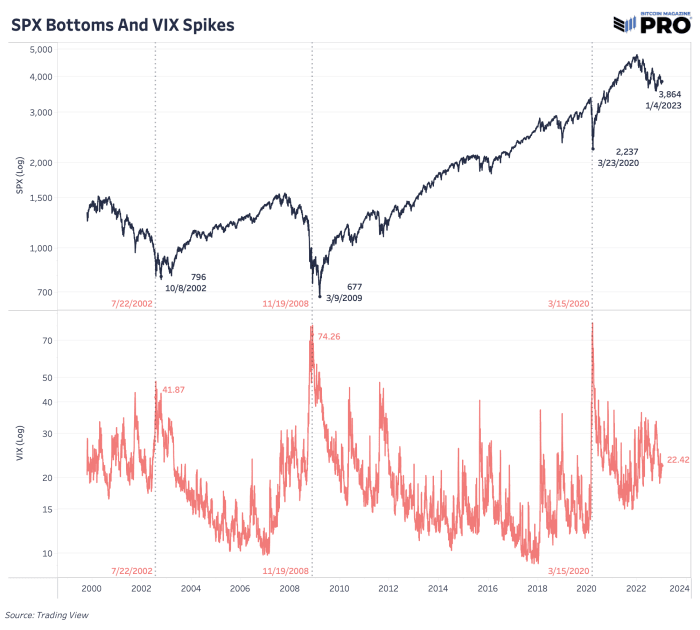

SPX Bottoms

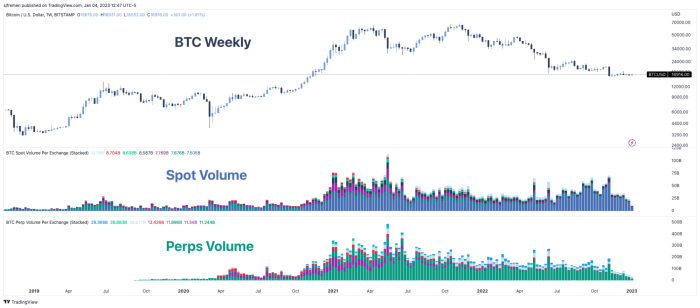

While there are different ways to define, classify and estimate the volume of bitcoins in the market, they all point to the same thing: September and November 2021 are the peak months of action. Since then, the volume in the spot market and the futures market has continued to decline.

Bitcoin volume in spot and futures markets

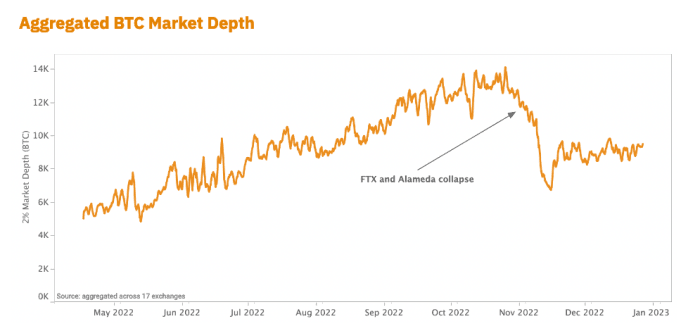

Overall market depth and liquidity have also been heavily impacted following the collapse of FTX and Alameda. The damage left a huge liquidity hole, which has yet to be filled due to the lack of market makers currently in place.

To date, bitcoin is still the most liquid market of any cryptocurrency or other “token”, but it is still relatively illiquid compared to other capital markets as the entire industry has been crushed in recent months. Market depth and lower liquidity mean assets are more volatile than shocks as relatively large single orders can have a greater impact on market prices.

Source: Kaiko Report Q4

Source: Kaiko Report Q4

Apathy On-Chain

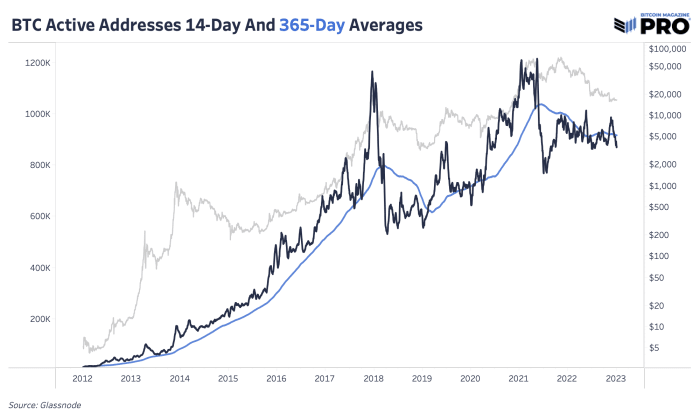

As expected in the current environment, we also see market complacency when looking at on-chain data. Although it continues to increase over time, the number of active addresses – unique addresses active as either a sender or receiver – has remained relatively stagnant over the last few months. The chart below highlights the 14-day moving averages of active addresses that have fallen below their moving averages over the past year. In the previous bull market situation, we have seen growth in the active address outpace style was quite significant.

Moving averages of active bitcoin addresses

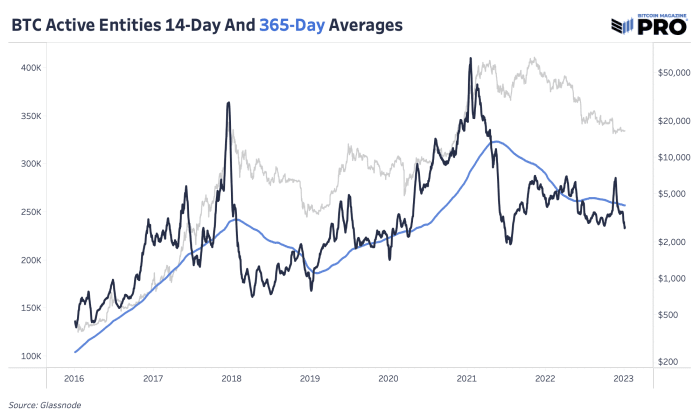

Because the address data is flawed, looking at the Glassnode data for active entities shows a similar trend. Overall, the bear market reversed as a result of many factors, including growth in new users and increased on-chain activity.

Moving average of active bitcoin entities

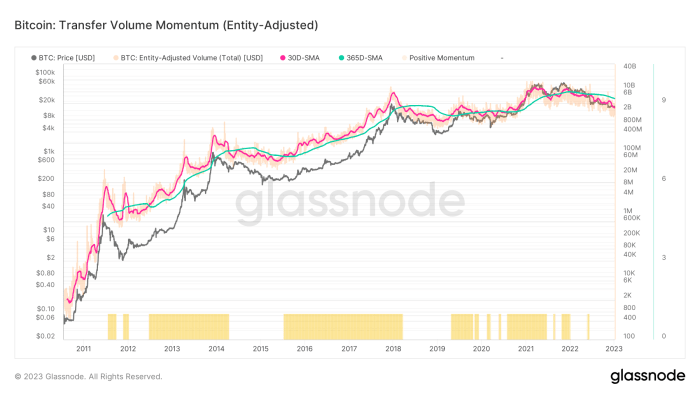

Bitcoin transfer volume momentum

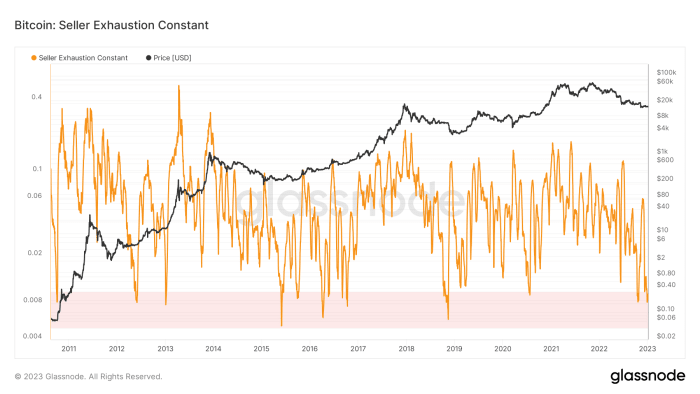

Bitcoin seller fatigue level

In our July 11 release “When Will the Bear Market End?”, we made the case that the burden of price-based capitulation has already been felt, while the real pain ahead is in the form of time-based capitulation.

“A look at previous bitcoin bear market cycles shows two distinct capitulation phases:

“The first was a price-based capitulation, through a series of sharp sales and liquidations, as the asset fell anywhere from 70 to 90% below its previous high.

“The second phase, and the one we often talk about, is the time-based capitulation, where the market finally starts to find the balance of supply and demand in the deep trough.” – Bitcoin PRO Magazine

We believe the capitulation is based on the present time. While the exchange rate pressure can certainly increase in the short term – due to the remaining macroeconomic pressures – the situation that seems to remain in the short and medium term appears to be a continuous period with a very low level of volatility that leaves both traders. and HODLers question when volatility and exchange rate appreciation will return.

Enjoy this content? Subscribe now to receive PRO articles directly in your inbox.