Downward trajectory: As consumers and businesses bounce back from tough times, insurers aren’t sure if there’s room for growth.

GDP data released by Statistics South Africa last week signaled a potential economic downturn this year, which is expected to suffer the slowest growth since the 2020 pandemic recession.

As in the fourth quarter of last year, which saw the economy shrink by 1.3%, the burden reduction will continue to weigh on growth, hindering the prospect of reducing the country’s highest unemployment rate.

Meanwhile, consumers have been left out of high inflation and higher interest rates.

One of the interesting characteristics of the GDP data is the revelation that financial services – the largest economic sector in the country – experienced the deepest contraction since the second quarter of 2020. the end of the year, especially behind the lower economic activity in financial intermediation, pension funds and insurance.

The weakness in the sector reflects the level of tension in businesses and consumers amid the recent recession, which threatens to disrupt the income of strained clients.

This week, Old Mutual became the latest insurer to signal the effects of low growth and higher inflation on its business.

Old Mutual’s headline earnings rose 10% to R7.9 billion for the year ending December 2022, according to the group’s financial results, released on Tuesday. But chief executive Iain Williamson pointed to difficult economic conditions for customers and the industry’s potential for growth.

He highlighted the many knocks the economy has suffered since the Covid-19 pandemic, including the 2021 civil unrest, last year’s devastating floods in KwaZulu-Natal, high inflation, higher interest rates and burden cuts. These factors, including a slow job recovery, had a negative impact on real income growth, he said.

“This downward pressure on disposable income growth, combined with depressed confidence, makes it difficult for customers to maintain or increase their contributions to protection, savings and investment products.

“The growth rate and liquidity of our corporate customers were also negatively impacted,” Williamson said.

Old Mutual’s personal finance and wealth management segment appears to have suffered the worst, as the value of new business fell 47% last year compared to 2021.

“The continuing effects of the macro-economic environment on customers’ ability to maintain or increase protection, savings and investment products will remain a challenge in 2023,” notes Old Mutual’s results. “We will continue to lead sales activities and the right mix in personal finance to accelerate our market share.

“However, there is uncertainty about whether the industry market as a whole will grow in the current economic environment.”

This statement by Old Mutual comes a week after Momentum Metropolitan’s interim results, which contained similar concerns about its ability to expand amid severe economic problems.

The insurer reported a 46% jump in normalized headline income to R2.2 billion for the six months ending December 31, 2022 and profit doubled to R1.9 billion over the period.

But the group’s growth was marred by weakness in investment and non-life-insurance business. Momentum Investments, according to results, reported lower operating earnings, mainly due to lower revenue on the Momentum Wealth platform, driven by lower new business volumes and weak market performance.

The group further reported its current value of new business premiums fell to R33.3 billion, 10% lower than the previous period. Momentum Investments experienced a 17% decline in the present value of new business premiums amid lower new business volumes on local and international wealth platforms.

“As a general trend, difficult economic conditions appear to have negatively impacted sales volume,” the results noted.

New pressure on sales volume is a concern, the company added.

“Disposable income remains under pressure due to rising interest rates and high inflation, as well as the lack of economic growth in South Africa. This may put pressure on affordability in new business volumes, particularly for long-term savings and protection businesses.

The chief executive of Momentum Metropolitan Hillie Meyer signaled this crisis in the group’s integrated results last year, saying: “I am worried about the socio-political situation facing the country and it will become increasingly difficult to increase income if there is no meaningful economic growth.”

It is difficult to reconcile the fourth quarter GDP figures with the generally strong financial results reported by companies in the financial services sector, said Patrice Rassou, chief investment officer at Ashburton Investments.

“So they still have a lot… But where we see some strain is at the bottom of the market, the mass market. There are some signs of emerging strain, which is quite clear. If you look at the insurance companies, the corporate sector has recovered and the top end has recovered, which can be seen in the Discovery numbers,” said Rassou.

Discovery, which supplies the top end of the market, reported a 15% jump in new business in the six months to 31 December.

“So, it’s not uniform. You have to look at the segment to see what’s going on.

The headwinds in the insurance industry are complex and include active volatility in the investment market at the end of Russia’s war in Ukraine, said Nishen Bikhani, partner at KPMG South Africa. In addition, rising inflation and high energy prices are having a negative impact on already strained consumers.

Bikhani says there is a huge gap in South Africa between those who can provide protection insurance and those who cannot.

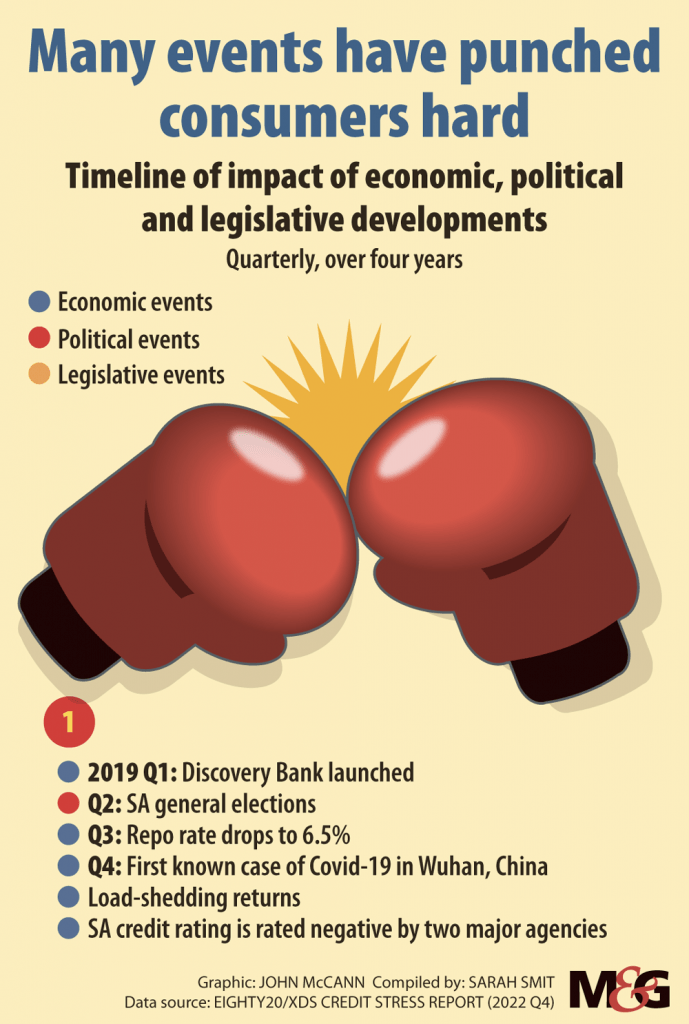

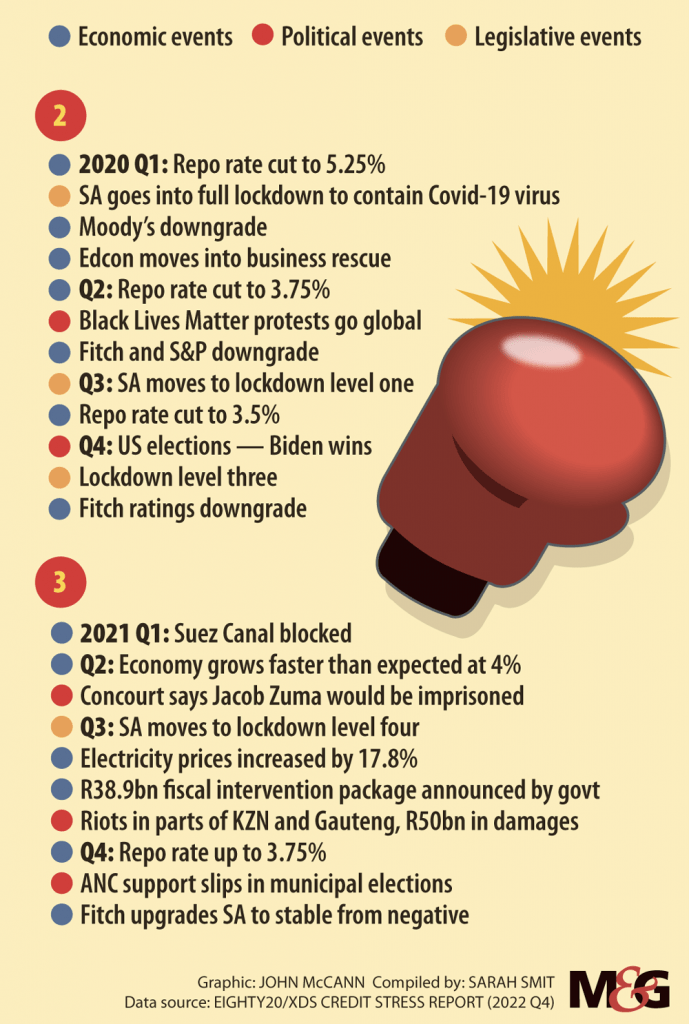

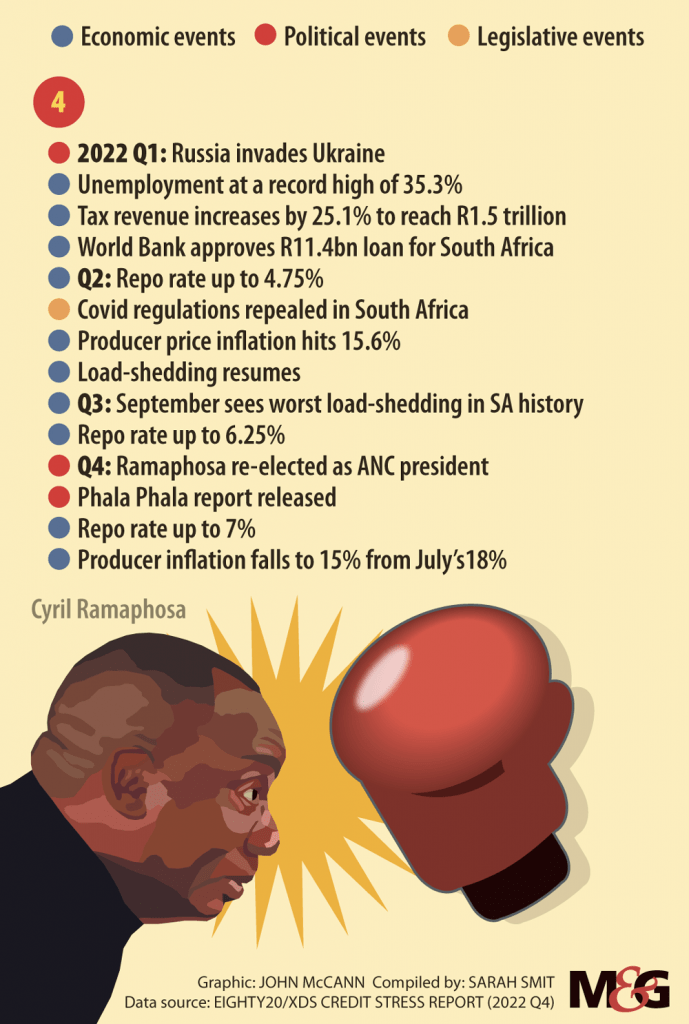

The latest data has shown the level of pressure on consumers in tighter financial conditions. The so-called mass segment, according to Eighty20’s credit stress report for the fourth quarter of last year, saw credit card balances balloon by R2.5 billion last year – indicating a reliance on credit for everyday purchases.

The average loan installment of this segment takes more than a third of their monthly income.

The middle class is also facing increased pressure. The segment’s average installment-to-income ratio increased by 7.4% over the past year and now stands at 69.4%. That means more than two-thirds of the average middle-class salary goes toward paying off debt, the data analytics firm said.

The KPMG Insurance CEO Outlook highlighted that insurance companies are actively developing strategies to respond to the pressures facing consumers, according to Bikhani.

“Insurance CEOs have prepared themselves and their organizations to deal with today’s economic and geopolitical challenges while exploring how to mitigate the impact of the recession,” he said. Therefore, Bikhani believes that the performance of insurance companies will rally, although they may continue to experience hits in the short and medium term.

In November, the South African Reserve Bank cited slow and uneven economic growth as a risk to financial stability, noting that unemployment and low incomes are reducing demand for financial services, credit and financial access.

Limited progress in implementing structural reforms leaves the economy vulnerable to periods of weak, unfair growth, the Reserve Bank’s financial stability review noted.

In January, the Reserve Bank posted a gloomy view of the country’s growth trajectory, forecasting growth of just 0.3% this year. Although the treasury forecast is slightly better, it only predicts growth of 0.9% this year.

Inequitable growth also increases “the risk of populist policies and social instability, which may have a negative impact on investor confidence, funding costs, insurance claims and operational costs”, the Reserve Bank said.